US Gulf:

NOLA urea barges dropped as low as $375/st FOB in early-week trading, the first time the market was recorded trading below $400/st FOB since June 2021. After the fall, prices gained some strength and were reported rising into the $395-$408/st FOB range later in the week. The week-ago range was $416-$455/st FOB. Sources cited the absence of an India tender for the weakness.

US Imports:

November urea imports totaled 563,686 st, off 28.1% from the year-ago 784,039 st. July-November volumes were counted at 1.33 million st, a 45.0% decrease from the prior 2.43 million st.

July-November imports from Qatar were 434,086 st, followed by 262,463 st from Saudi Arabia. Oman moved ahead of Canada’s 136,053 st fertilizer year-to-date total with 236,512 st, while Russia added 126,834 st.

US Exports:

November urea exports moved 165.3% higher year-over-year, to 67,750 st from 25,541 st. July-November totals were up 784.1%, to 769,233 st from 87,005 st noted one year earlier.

Eastern Cornbelt:

Driven by a significant drop in NOLA barge prices during the week, urea terminal prices fell to $480-$500/st FOB in the Eastern Cornbelt, some $40/st below the prior week. The Cincinnati, Ohio, market was reported in the $485-$500/st FOB range at midweek.

Western Cornbelt:

Plunging urea prices fueled by softening NOLA barge values pushed terminal pricing down to $455-$500/st FOB in the Western Cornbelt, well below the prior week’s $510-$530/st FOB range, with the high confirmed in Iowa and the low at St. Louis, Mo.

Southern Plains:

Following a plunge in NOLA barge prices on Jan. 10, urea at Catoosa/Inola, Okla., fell from a high of $500/st early in the week to a low of $450-$460/st FOB. The Houston, Texas, urea market was pegged at the $495/st FOB level at midweek.

South Central:

A sharp drop in NOLA barge prices on Jan. 10 fueled a downward shift in urea terminal prices in the region. While the week began with prices at the $515/st level FOB Memphis, Tenn., sources said $480-$495/st FOB was more common out of river terminals by midweek, with a low of $450/st FOB confirmed at Convent, La., on Jan. 11. Sources noted, however, that very little new business was being done on urea.

Southeast:

Urea offers were quoted at $510/st FOB Wilmington, N.C., and Norfolk, Va., down significantly from the $590/st FOB levels reported in mid-December. No urea was available in the Savannah, Ga., market in early January.

India:

Sources are now convinced there will be no spot tender call until mid-February. One trader noted that the country will first want to get past the IPL tender call for 600,000 mt to be delivered over a one-year period.

The IPL tender will close Jan. 23 and represents the first time one of the major Indian importers issued a tender of this type. IPL is asking for a commitment of at least one cargo per month through February 2024, with each shipment to be priced at a discount to market values. The tender is open only to producers.

Media reports indicated that the rising price of natural gas in India could reduce domestic production. Sources said that even if production is not affected, the higher production cost will most likely require additional funding for the government’s urea subsidy program. Urea already accounts for about one-third of the program’s total fertilizer subsidy expenditures.

Proposals for the 2023-2024 fiscal-year budget are being floated. If the current plans to reduce subsidies for urea and other fertilizers are enacted, local economists reportedly told local newspapers that farmers will either cut back on fertilizer purchases, leading to reduced crop output, or pass on the higher costs to food buyers. Either way, the increases in food costs could push inflation rates even higher, the economists said.

Black Sea:

Sources estimated that the prilled urea price from the Black Sea dipped to $370-$405/mt FOB.

Indonesia:

Sources reported that major producers are focusing their attention on the domestic market through February. Once exports are opened up, it appears that producers will be permitted to ship out 1 million mt in 2023, sources said.

Middle East:

Players put the market out of the Arab Gulf at $420-$440/mt FOB, but with only limited business as a guide. Sources reported that a small cargo from Qatar, sold to a Turkish buyer at $430/mt FOB, was the only public deal.

OMIFCO shut down one ammonia-urea line for 25 days for routine maintenance. The routine closure will leave the company with only one spot cargo available for shipment in February. The rest of the remaining output is already booked under long-term contracts.

Egyptian producers have once again gone quiet. No new deals from Egypt were reported, despite earlier hopes by producers to push the price past the $510/mt FOB level set at the beginning of the month.

Sources reported that availability of urea from Iran remains limited, and restrictions on natural gas availability have forced producers to cut back on tons being offered. Even as supplies are tight, sources reported softer prices. Offers of $410/mt FOB were reportedly floated, down from the $450/mt FOB discussed as the year began.

January-November urea exports were counted at 4.6 million mt, Trade Data Monitor reported, up about one-third from the 3.5 million mt exported through the same period in 2021. The main buyers were Turkey with 1.7 million mt, and South Africa with 553,000 mt.

November exports were reported at 448,000 mt, up dramatically from 267,000 mt shipped in November 2021. Turkey accounted for 52% of exports with 235,000 mt, while Thailand, South Africa, and China took about 62,000 mt each.

China:

Sources said that limited tonnage is available for export. Some traders noted preparations were already underway to celebrate the Lunar New Year, beginning on Jan. 22. The Chinese government usually grants a full week off for the holiday, although many companies give workers additional time to celebrate.

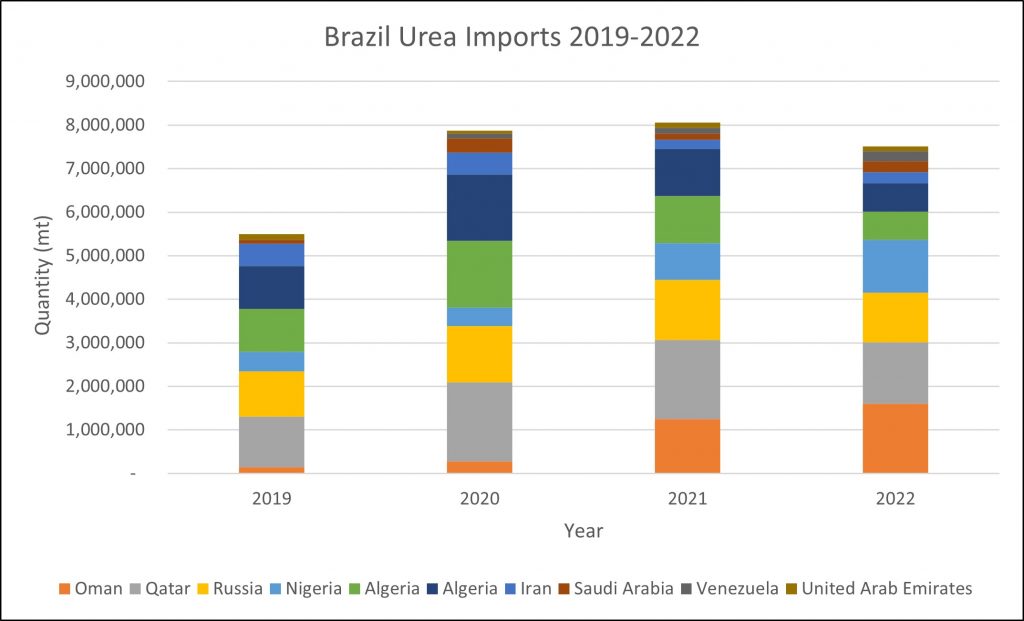

Brazil:

The lackluster global market is having an impact on Brazil, and prices have softened to $445-$460/mt CFR. Unconfirmed reports put bidding as low as $430/mt CFR, with no takers so far.

Urea from Venezuela was reported getting bids at $420/mt CFR. Venezuela and Iran were noted among sanctioned countries offering their product for significant discounts. So far, it does not look as if the holder of the Venezuelan material has accepted the low bids.

The range in Rondonopolis widened to $590-$660/mt FOB ex-warehouse. Sources said the upper end came from sellers with no urgency to move product, while the lower end was holders of product looking for prompt shipment.

Urea imports for 2022 were down slightly from 2021, according to Trade Data Monitor. Imports were reported at 7.2 million mt, off from 7.8 million recorded in 2021. The two top suppliers were Oman with 1.6 million mt and Qatar with 1.4 million mt. Nigeria shot up to third place with 1.2 million mt, a 44% increase from 2021.

December imports totaled 710,000 mt, up marginally from the year-ago 680,000 mt. Oman accounted for about one-third of the December market with 203,000 mt.

Fourth-quarter imports were down 17%, falling to 2 million mt from 2.4 million mt 2021. Second-half imports totaled 4.1 million mt, slightly below the year-ago 4.3 million mt.

Ethiopia:

Urea imports totaled 457,000 mt for 2022, according to Trade Data Monitor, down 14% from 531,000 mt imported in 2021. Ethiopia’s main suppliers were Egypt with 355,000 mt, followed by the United Arab Emirates with 100,000 mt

Imports were negligible in December and the fourth quarter. Trade Data Monitor reported zero imports in both December 2021 and December 2022, while fourth-quarter 2022 imports totaled just 301 mt, down significantly from 100,000 mt in the prior-year period.

Second-half 2022 imports were pegged at 111,000 mt, off from 188,000 mt in second-half 2021. The bulk of Ethiopian urea imports usually arrives in the first six months of the year.