Central Florida:

DAP trucks loading from Central Florida remained posted at $650/st FOB, steady from the prior report. MAP trucks were also noted at $650/st FOB, unchanged from one week earlier.

North Florida MAP trucks were priced at $700/st FOB, sources said.

US Gulf:

Sources reported a mixed NOLA phosphate market, with DAP barges firming from week-ago levels while MAP softened from its recent top.

Domestically-produced DAP barges reportedly changed hands at $625/st FOB for January and February loading, steady from the prior high, while players typically noted the weekly floor firming to $620/st FOB, a $5/st increase from the previous $620/st FOB. Players also reported $620/st FOB pricing in the DAP paper market.

MAP barges were seen ticking lower, however, with domestic tonnage trading at $610/st FOB, shy of week-ago price ideas quoted up to $620/st FOB. Most put the bottom of the range at $605/st FOB, even with the prior MAP floor.

NOLA DAP barges loading in January and February were noted trading in a $620-$625/st FOB range for the week, rising from $615-$625/st FOB at last check. MAP barges were tabbed at $605-$610/st FOB, below the week-ago $605-$620/st FOB.

US Imports:

November DAP imports softened 21.9% from the prior year, to 61,703 st from 79,046 st. Imports fell 52.4% st for July-November, to 318,619 st from the year-ago 668,785 st.

Saudi Arabia led July-November imports with 218,741 st, followed by Australia with 80,479 st and 12,534 st from Russia.

MAP/Other imports were off 19.8% in the July-November period, falling to 381,110 st from 475,436 st in the prior-year period. Imports moved 46.5% lower in November, to 91,788 st from the year-ago 171,674 st.

Imports from Russia totaled 115,165 st in July-November. Saudi Arabia added 90,281 st, followed by 86,427 st from Australia. Mexico sent 43,592 st.

US Exports:

November DAP exports moved 65.8% lower, to 38,957 st from the year-ago 113,839 st. July-November exports were up 21.7%, however, to 342,285 st from 281,152 st.

MAP/Other exports fell 9.2% in July-November, to 765,777 st from the year-ago 843,184 st. Export shipments totaled 143,883 st for November, however, a 23.0% increase from 117,020 st in the prior November.

Sources reported a 5,000 mt MAP sale destined into a single destination in northern Latin America. The cargo, priced within the market’s recent $640-$670/mt FOB range at $650/mt FOB, was scheduled to ship near the end of January.

Based on reported trades, the US Gulf export phosphate markets shifted to $650/mt FOB from the week-ago $640-$670/mt FOB.

Eastern Cornbelt:

DAP offers were quoted at $680-$690/st FOB in the Eastern Cornbelt, down $5-$15/st, with the Cincinnati market pegged in the $680-$685/st FOB range. MAP pricing slipped to $675-$685/st FOB in the region, with the low at Cincinnati and the high at Ottawa.

Western Cornbelt:

DAP pricing dropped $670-$680/st FOB in the Western Cornbelt, with the St. Louis market quoted at $670-$675/st FOB. MAP was reported in the same range as DAP during the week.

Southern Plains:

DAP was quoted at $670-$685/st FOB Catoosa/Inola, down $5-$10/st, with MAP reported in the $660-$670/st FOB range at that location, reflecting a $10/st drop. The Houston market was pegged at $685/st FOB for DAP and $675/st FOB for MAP at midweek.

South Central:

DAP pricing in the South Central region was quoted at $680-$690/st FOB, down $20-$25/st from last report.

Southeast:

MAP pricing from Nutrien remained at $700/st FOB Aurora, N.C., and White Springs, Fla.

China:

Major DAP producer YUC was said to be in steady talks with buyers looking for the limited tonnage the company has to offer for sale. Sources said a completed deal of $680/mt FOB is now too high for the current market, and most of the discussion seems to have centered on $620-$650/mt FOB. So far nothing has been reported at that level, but sources said it is only a matter of time before the lower pricing is achieved.

Brazil:

Sources said MAP prices remained stable at $650-$670/mt CFR. There were reports of buyers pushing for a drop of $5/mt on the upper end, but nothing was confirmed at that level. Sources said the lower end of the range appeared to be dominated by Russian and Chinese material.

Rondonopolis showed a slight dip to $780-$810/mt FOB ex-warehouse. The price change was seen more as a routine fluctuation than as the harbinger of a major price shift.

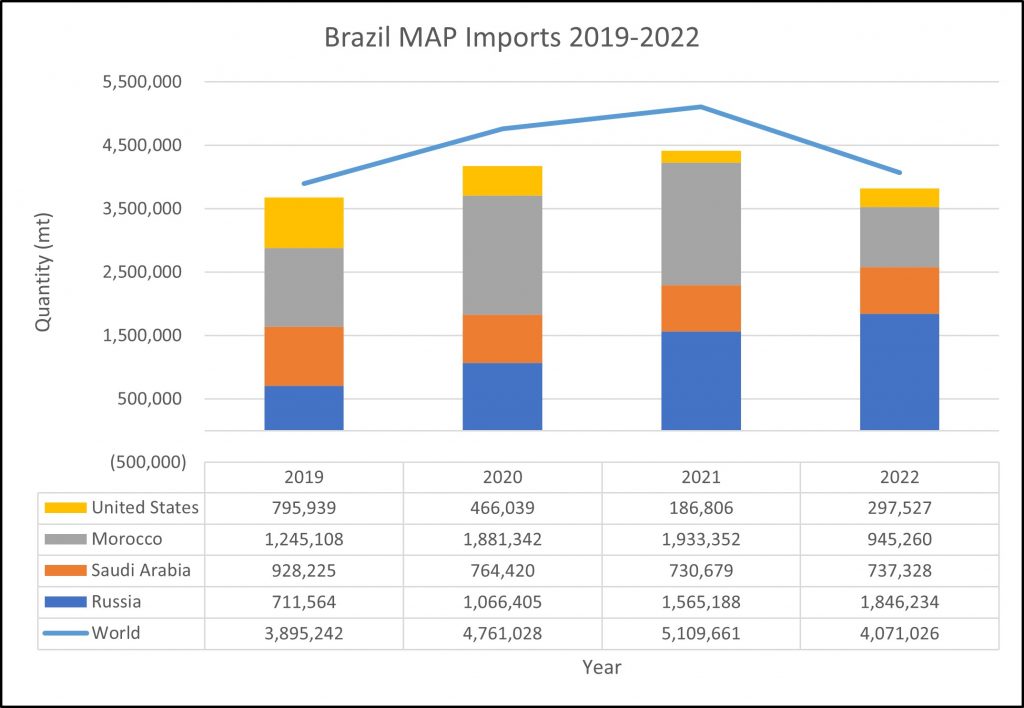

MAP imports for 2022 fell about 1 million mt year-over-year, according to Trade Data Monitor, to 4.1 million mt from 5.1 million mt. Russia sent 1.8 million mt, followed by Morocco with 945,000 mt.

December MAP imports were pegged at 234,000 mt, down 44% from 418,000 mt in December 2021, with Russia’s 210,000 mt accounting for 91% of the market. Fourth-quarter imports fell to 684,000 mt versus the prior-year 1.5 million mt, while second-half imports were reported at 1.9 million mt, off from 3.1 million mt.