California:

Potassium nitrate pricing in California remained at $1,145/st FOB Stockton for bulk, $1,240/st FOB for bulk bags, and $1,260/st FOB for 50-pound bags.

California:

Potassium nitrate pricing in California remained at $1,145/st FOB Stockton for bulk, $1,240/st FOB for bulk bags, and $1,260/st FOB for 50-pound bags.

Eastern Cornbelt:

The potassium thiosulfate market continued at $650/st FOB Terre Haute in mid-August.

Western Cornbelt:

Potassium thiosulfate pricing remained at $650/st FOB Waterloo, Iowa.

California:

The potassium thiosulfate market dropped to $650/st FOB Sacramento, down $30/mt from July.

Eastern Cornbelt:

Most of the Eastern Cornbelt enjoyed dry weather and comfortable temperatures in the 80s during the week, but an increased chance of storms was likely late in the week and into the weekend.

Forecasts warned of strong storms with hail and damaging winds in northern Illinois on Aug. 15-16, while the National Weather Service in Indianapolis, Ind., on Aug. 15 issued a severe weather warning for the weekend, with flash flooding possible in some locations.

Similar forecasts were in place for central and northern Ohio, with widespread rain and thunderstorms expected on Aug. 16-17 and highs topping out in the mid-80s. Severe storms were also in Michigan’s forecast on Aug. 16.

USDA on Aug. 11 rated 72-76% of the corn and soybeans in Illinois as good or excellent, along with 68-69% of the acreage in Indiana, 59-62% in Ohio, and 56-59% in Michigan.

Western Cornbelt:

Another round of heavy rain churned through western and central Iowa on Aug. 14-15, with nearly four inches reported in Winterset and more than two inches falling in locations such as Iowa City, Quad Cities, Lorimor, and Clarinda.

Multiple Nebraska locations also collected more than two inches of rain as the system pushed through the region, including Ralston, Springfield, and Omaha, while Council Bluffs and Fremont each saw more than an inch of rainfall at midweek.

The National Weather Service also warned of the potential for severe weather in central Missouri on Aug. 15, with forecasts warning of damaging winds, large hail, and possible tornadoes.

Crop conditions remained very favorable in the region, with good or excellent ratings assigned to 77-81% of the corn and soybeans in Missouri and Iowa and 69-71% in Nebraska. Missouri’s rice crop and cotton were 71% and 55% good or excellent, respectively, while 70% of Nebraska’s sorghum crop fell into those two categories at mid-month.

California:

Hot summer weather continued across California in mid-August, though the triple-digit highs of recent weeks have moderated a bit, and spotty thunderstorms were reported across Northern California.

The massive Park Fire, California’s largest wildfire so far this year and the fourth largest on record in the state, was 40% contained on Aug. 14 after scorching more than 670 square miles. A large portion of the fire is within Lassen National Forest, with major impacts reported in Butte and Tehama counties.

Other major fires in California had significant levels of containment at mid-month, except for the Aug. 9 Boise Fire in Six Rivers National Forest, which had covered more than 11 square miles by midweek.

California’s cotton crop was 100% good or excellent as of Aug. 11, with 70% of the acreage setting bolls by that date. The state’s rice crop was 95% good or excellent.

Pacific Northwest:

Temperatures moderated considerably across the Pacific Northwest in mid-August, though heavy smoke was still a factor in most locations due to numerous wildfires in the region and in western Canada.

Strong thunderstorms were reported in the Klamath Basin at midweek, with reports of gusty winds and marble-sized hail. Frequent thunderstorms also rolled through parts of Idaho and western Montana during the week, bringing brief but heavy rain to some locations.

The small grains harvest was well underway in the region. Oregon growers had 83% of the winter wheat crop in the bin by Aug. 11, compared with 69% in Montana, 66% in Washington, and 48% in Idaho. The spring wheat and barley harvest was 32-38% complete in Washington, 19-22% in Montana, and 17-19% in Idaho, with good or excellent ratings assigned to 63-79% of the acreage in Idaho, 58-59% in Montana, and just 17-21% in Washington.

Western Canada:

A strong storm on Aug. 12 brought large hail and heavy rain to parts of southern Alberta, including reports of hail damage to some crops that were nearly ready to harvest. Nearly all of the state was also under an air quality advisory in mid-August due to smoke from multiple wildfires in the region.

Manitoba growers had 17% of the winter wheat crop and 39% of the fall rye harvested by Aug. 13, with combining also underway on barley, field peas, and spring wheat. Harvest progress was tracking slightly ahead of the average pace in Saskatchewan, with 6% of all crops in the bin across the province and up to 16% in southwestern Saskatchewan.

Alberta growers are expecting an average crop this year after hot, dry weather in July. Currently 51% of all crops in the province are rated as good or excellent, below the five- and ten-year averages of 56% and 59%, respectively.

US Gulf:

Northbound loading drafts were reduced by 5% on travel above New Orleans during the week due to reduced water levels on the Lower Mississippi River.

Travel was unavailable through Port Allen Lock on Aug. 12-15 to facilitate the completion of repairs begun in March. The site was closed for most of April following a miter gate hinge anchorage failure on March 28.

Vessels detoured through Algiers Lock during the Port Allen Lock shutdown, prompting delays up to 23 hours on Aug. 15. Dredging reported in the New Orleans Harbor was scheduled to continue through Aug. 26.

Guidewall repairs at Bayou Sorrel Lock are set to continue through Oct. 30, limiting travel from 7 a.m. to 4 p.m. daily. Intermittent waits were noted up to seven hours, falling from 25 hours at last report.

Repairs at Brazos Lock halted weekday travel between 7 a.m. and 7 p.m. Most transits topped out around 5-11 hours, though a handful of waits were noted up to 30 hours. The project is scheduled to run through October.

Harvey Lock will see intermittent shutdowns from 7 a.m. to 6 p.m. on Aug. 19-21, with a brief opening planned daily from 1-2 p.m. The lock will shut again from 7 a.m. to 12 p.m. on Aug. 22. Potential reverse head conditions in the forecast for late August could force a complete closure, sources warned.

Industrial Lock waits were quoted at 5-13 hours during the week, while tows waited up to nine hours to pass Harvey Lock. Colorado Lock transits ran up to six hours, Corps data indicated.

Mississippi River:

Low water levels forced draft reductions on the lower river, sources noted. Northbound drafts were cut by 5% between New Orleans and Cairo, Ill., while drafts were reduced by 5-10% on southbound travel between Cairo and Rosedale, Miss.

Dike work at Mile 759 triggered daily southbound shutdowns between 7 a.m. and 7 p.m. The project is anticipated to run through Sept. 18, with no impact to upriver travel expected.

Pipeline removal at Mile 158 will run from Aug. 18 through Sept. 24. No shutdowns are expected, but channel restrictions could slow travel while work is underway, sources said. Dredging is underway at Mile 154 until further notice, according to a Corps posting.

Revetment work at Mile 908 will block downriver travel during daylight hours on Sept. 1-5, while dates for a planned revetment operation at Mile 775 are expected to be finalized in late August. That project will also limit daytime movements in the southbound direction while work is underway.

Sporadic nine-hour delays were reported at Lock 10 during the week, and intermittent 4-9 hour waits were noted at Lock 24. Lock 25 delays were quoted up to 11 hours. Lock 21 was closed to navigation on Aug. 13, sources noted.

Final release dates for NOLA-loaded barges destined for upper-river ports between Dubuque, Iowa, and St. Paul, Minn., were expected in the first week of October. Tows departing NOLA for ports between St. Louis and Clinton, Iowa., were projected to see final departures in the third week of October. Upper-river locks will undergo seasonal closures between December and March 2025.

Illinois River:

Maximum loading drafts continued at 9.5 feet for Miles 1-231 and 9.0 feet above Mile 231 on the Illinois River.

Lockport Lock is scheduled to shut completely on Jan. 14-March 11, 2025, for vertical lift gate installation, blocking travel to and from the Chicago area. Lockport Lock is located at Mile 291.

Ohio River:

Towing reductions continued on the Ohio River, sources said. Drafts were reduced by 5-10% depending on location and direction of travel.

The Markland Lock main chamber is offline for 19 hours daily through Aug. 30, forcing detours through the secondary chamber. The lock is scheduled to close once more between Sept. 8 and Oct. 6. Delays were quoted in the 4-20 hour range during the week.

The Hannibal Lock main chamber is offline for miter gate repairs through Nov. 8, prompting waits up to 26 hours. McAlpine Lock is shut to southbound travel from 7 a.m. to 7 p.m. through Nov. 30, with delays reported up to 13 hours.

The primary chamber at John T. Myers Lock is slated to close from Aug. 21 through Nov. 9, with long delays expected. Belleville Lock will experience a round of 30-day main and auxiliary chamber shutdowns before the end of the year.

Delays were reported up to 23 hours at the Tennessee River’s Kentucky Lock. Wait times ran up to 14 hours at both Pickwick Landing Lock and Wilson Lock during the week.

Construction at Lock 3 of the Monongahela River will effectively close the river to commercial navigation through approximately Aug. 25, sources said.

Arkansas River:

Van Buren Bridge repairs scheduled for Aug. 22 through Sept. 8 will completely close the site to navigation. The Corps is said to be planning a single opening to pass queued vessels sometime after the ninth day of work, though shuttle barges will be free to pass whenever the channel is free of equipment.

Webbers Falls Lock is scheduled to close from Aug. 26 through Sept. 8 for miter gate inspection. Sporadic delays and shutdowns are expected leading up to the closure.

The Mosaic Co. reported a second-quarter net loss of $162 million on net sales of $2.82 billion, down from net income of $369 million and sales of $3.4 million in last year’s second quarter. The quarterly loss was the company’s largest in five years, with Mosaic citing the impact of lower selling prices and margins.

Adjusted EBITDA fell to $584 million from $744 million last year, but beat the average analyst estimate of $576.4 million.

Lower pricing pressured potash operating earnings to $174 million for the quarter, down from $328 million last year. Adjusted EBITDA for the potash segment totaled $271 million, compared to $408 million last year, reflecting the impact of lower prices, partially offset by higher volume and lower costs per mt.

Net sales in the potash segment totaled $663 million, down from $849 million last year, while gross margin fell to $186 million from $336 million. Total potash production in the quarter was 2.2 million mt, up from 1.9 million mt last year, while potash sales volumes firmed to 2.3 million mt from 2.2 million mt last year.

Mosaic confirmed that it restarted its Colonsay mine in July to offset upcoming turnarounds at Esterhazy, and to meet what the company described as the “strong demand outlook as the market responds to the China and India contract settlements.”

Phosphate operating earnings for the quarter fell to $133 million from $146 million last year, while adjusted EBITDA for the segment dropped to $308 million from $385 million, with Mosaic citing lower sales volumes.

Phosphate net sales dipped to $1.2 billion from $1.3 billion last year, while phosphate sales volume totaled 1.7 million mt for the quarter, down 12% from last year. Phosphate production volumes were up 1%, however, to 1.7 million mt.

Mosaic Fertilizantes second-quarter earnings jumped to $61 million from an operating loss of $20 million last year. Adjusted EBITDA for the segment totaled $96 million during the quarter, up from $66 million last year, reflecting higher distribution margins.

Net sales for Mosaic Fertilizantes were $1.0 billion for the quarter, down from $1.4 billion last year due to lower pricing. Gross margin was $102 million, compared to $13 million for the same period last year. Mosaic said cash unit costs of mined rock, phosphate finished products conversion, and potash production all declined from the year ago period, reflecting the company’s focus on cost reduction.

Mosaic said potash sales volumes in the third quarter are expected to be in the range of 2.1-2.3 million mt, with realized mine-gate MOP prices in the $200-$220/mt range. Mosaic said its third-quarter potash pricing guidance reflects a higher mix of international volume. Phosphate sales volumes in the third quarter are expected to be in the 1.7-1.9 million mt range, with DAP prices at the plant projected at $555-$575/mt.

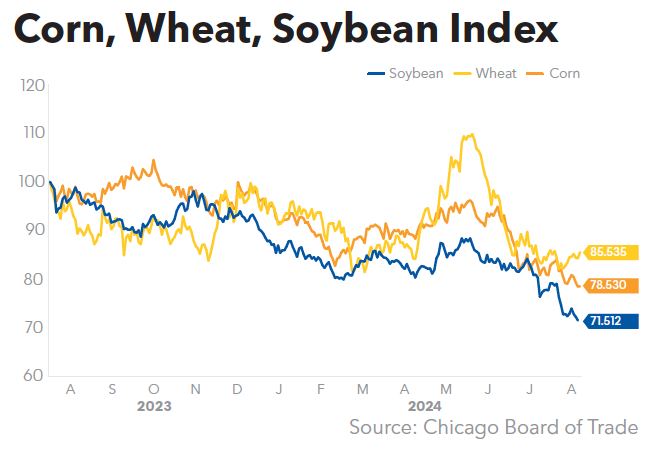

Looking ahead, Mosaic said low stocks-to-use ratios for grains and oilseeds are positives for agriculture fundamentals and should incentivize growers to maximize yields. While corn and soybean prices have softened, the company said nutrients remain affordable, which bodes well for fertilizer demand.

“North American demand is robust, with buyers seeking summer fill after emptying their bins this spring and Brazil in-season demand is solid on concerns of low stocks,” Mosaic said. The company said the long-term phosphate outlook remains favorable amid a 27% year-over-year decline in Chinese exports, while the recent potash contract settlements in China and India “should stimulate buying activities further in Southeast Asia and India.”

“These factors suggest the global potash market is balanced and the phosphate market will remain tight in 2024 and beyond,” Mosaic said.

Mosaic highlighted progress on a number of “low-capital-intensity projects,” include the addition of 800,000 mt of MicroEssentials capacity at its Riverview, Fla., facility; the completion of a potash compaction project at Esterhazy that allows the conversion of standard MOP to granular products, as well as a project to add 400,000 mt of milling capacity at Esterhazy, which is on track for completion in mid-2025; and the construction of a 1 million mt blending facility in Palmeirante, Brazil, which is on track for completion in 2025.

The company also highlighted progress on a cost reduction plan announced last year, and said it has achieved more than one-third of the targeted $150 million run rate compared to the 2023 baseline. Mosaic said it is on track to reduce 2024 capital expenditures by $200 million from 2023 levels.

Nutrien Ltd. reported second-quarter net earnings of $392 million ($0.78 diluted net earnings per share) and adjusted EBITDA of $2.24 billion, down from $448 million ($0.89 diluted net earnings per share) and $2.48 billion, respectively, in last year’s second quarter. The EBITDA results were up slightly from the average analyst estimate of $2.2 billion.

Nutrien cited lower fertilizer net selling prices and a loss on foreign currency derivatives, partially offset by increased Retail earnings, higher offshore potash sales volumes, and lower natural gas costs.

“Nutrien benefited from improved Retail margins, higher fertilizer sales volumes, and lower operating costs in the first half of 2024,” said Ken Seitz, Nutrien President and CEO. “Our upstream production assets and downstream Retail businesses in North America and Australia have performed well in 2024.”

Nutrien said sales volumes were lower in the second quarter as wet weather in North America impacted the timing of nitrogen applications, while first-half sales volumes were flat from 2023.

Net selling prices were lower in the second quarter and first half for all major nitrogen products, the company said, primarily due to weaker benchmark prices in key nitrogen producing regions. Cost of goods sold per mt decreased in the second quarter and first half mainly due to lower natural gas costs.

Nutrien reported net earnings of $557 million and adjusted EBITDA of $3.3 billion for the first six months, down from last year due to lower fertilizer prices but partially offset by increased Nutrien Ag Solutions earnings, higher potash sales volumes, and lower natural gas costs.

Retail adjusted EBITDA increased to $1.2 billion in the first half supported by strong demand and a normalization of product margins in North America. Nutrien lowered its Retail adjusted EBITDA guidance to $1.5-$1.7 billion, however, due primarily to ongoing market instability in Brazil and the impact of delayed planting in North America in the second quarter.

Potash adjusted EBITDA declined to $1.0 billion in the first half due to lower prices, which more than offset higher sales volumes and lower operating costs. Potash sales volume guidance was raised to 13.2-13.8 million mt due to record first-half sales volumes and the expectation for strong global demand in the second half, Nutrien said, adding that the range “reflects the potential for a relatively short duration Canadian rail strike in the second half.”

“The settlement of contracts with China and India in July is expected to support demand in standard grade markets in the second half of 2024, while uptake on our summer fill program in North America has been strong,” the company said.

Nitrogen adjusted EBITDA decreased to $1.1 billion in the first half due to lower prices, which more than offset lower natural gas costs. The company narrowed its nitrogen sales volume guidance to 10.7-11.1 million mt based on expectations of higher operating rates at its North American and Trinidad plants and growth in sales of urea and UAN. Nutrien said its ammonia production increased in the first half, driven by improved reliability and less turnaround activity.

“Chinese urea export restrictions have been extended into the second half of 2024 and natural gas-related supply reductions could continue to impact nitrogen operating rates in Egypt and Trinidad,” the company said. “US nitrogen inventories were estimated to be below average levels entering the second half of 2024, contributing to strong engagement on our summer fill programs.”

Phosphate adjusted EBITDA decreased in the second quarter and first half primarily due to lower prices, partially offset by lower input costs. Phosphate sales volume guidance was lowered to 2.5-2.6 million mt reflecting extended turnaround activity and delayed mine equipment moves.

“Phosphate fertilizer prices are being supported by tight global supply due to Chinese export restrictions, low channel inventories in North America, and seasonal demand in Brazil and India,” Nutrien said. “We anticipate some impact on demand for phosphate fertilizer in the second half of 2024 as affordability levels have declined compared to potash and nitrogen.”

Nutrien said favorable growing conditions have created an expectation for record US corn and soybean yields and pressured crop prices. “Despite lower crop prices, demand for crop inputs in North America is expected to remain strong in the third quarter of 2024 as growers aim to maintain optimal plant health and yield potential,” the company said. “We anticipate that good affordability for potash and nitrogen will support fall application rates in 2024.”

Nutrien recognized a $195 million non-cash impairment of assets due to the company’s previously announced decision to halt its Geismar Clean Ammonia project (GM June 14, p. 1).

The company also highlighted is margin improvement plan in Brazil, which included the curtailment of three fertilizer blenders and the closure of 21 selling locations in the second quarter (GM May 31, p. 26). Nutrien recognized a $335 million non-cash impairment of its Retail-Brazil assets due to ongoing market instability and more moderate margin expectations, and incurred a loss on foreign currency derivatives of approximately $220 million in Brazil.

“In Brazil, we continue to see challenges and are accelerating a margin improvement plan that is focused on further reducing operating costs and rationalizing our footprint to optimize cash flow,” Seitz said.

Nutrien announced that its Board of Directors has declared a quarterly dividend of $0.54 per share payable on Oct. 18, 2024, to shareholders of record on Sept. 27, 2024.

CF Industries Holdings Inc. reported second-quarter net earnings of $420 million ($2.30 per diluted share) and adjusted EBITDA of $752 million, down from $527 million ($2.70 per diluted share) and $857 million, respectively, in last year’s second quarter.

Net sales for the quarter were $1.57 billion, down from last year’s $1.78 billion but up from the average analyst estimate (Bloomberg Consensus) of $1.52 billion. CF cited lower average selling prices compared with last year, with lower ammonia, UAN, and ammonium nitrate sales volumes partially offset by higher urea volumes.

For the first half of 2024, net earnings were $614 million ($3.31 per diluted share) and adjusted EBITDA was $1.21 billion, down from $1.09 billion ($5.55 per diluted share) and $1.72 billion, respectively, in 2023. First-half net sales were $3.04 billion, down from $3.79 billion, while sales volumes were similar to the first half of 2023.

Cost of sales for the second quarter and first half were lower than last year due primarily to lower realized natural gas costs, partially offset by higher 1Q maintenance costs related to plant outages. The average natural gas cost was $1.90 per MMBtu in the second quarter and $2.53 per MMBtu in the first half, compared to $2.75 per MMBtu and $4.56 per MMBtu, respectively, in 2023.

Gross ammonia production for the first half and second quarter was approximately 4.8 million and 2.6 million tons, respectively, compared to 4.7 million and 2.4 million tons last year. The company expects gross ammonia production for the full year 2024 to be approximately 9.8 million tons.

Ammonia net sales for the quarter were $409 million, down 22% year-over-year and slightly under the average analyst estimate of $409.2 million. Ammonia sales volumes came in at 979,000 st, down 7% from last year but above the analyst estimate of 978,472 st, while the average ammonia selling price was $418/st, down 16% year-over-year and trailing the analyst estimate of $421.11/st.

Granular urea net sales for the quarter were $457 million, down slightly from $460 million last year but above the average analyst estimate of $398.8 million. Granular urea sales volumes were 1.25 million st, up 9.1% from last year and above the analyst estimate of 1.15 million st, while the average selling price of urea came in at $365/st for the quarter, down 9% from last year but above the analyst estimate of $346.88/st

UAN net sales were reported at $475 million for the quarter, down 13% from last year but above the $456.7 million average analyst estimate. UAN sales volumes came in at 1.75 million st, down 3.4% from last year and only slightly trailing the 1.76 million st analyst estimate, while the average UAN selling price was $272/st for the quarter, down 10% from last year but ahead of the analyst estimate of $259.31/st.

Ammonium nitrate (AN) net sales were $98 million for the quarter, down 5.8% from last year and trailing the analyst estimate of $109.8 million. AN sales volumes were 340,000 st, down 7.9% from last year and below the 378,766 st analyst estimate, while the average selling price was reported at $288/st, up 2.1% from last year but trailing the $289.47/st analyst estimate.

Capital expenditures in the second quarter and first half were $84 million and $182 million, respectively, and the company projects capital expenditures for the full year to be approximately $550 million.

CF repurchased 4.0 million shares for $305 million during the second quarter and 8.3 million shares for $652 million during the first half of 2024. On July 31, 2024, CF’s Board of Managers approved a semi-annual distribution payment to CHS Inc. of $165 million for the distribution period ended June 30, 2024. The distribution was paid on July 31, 2024.

CF said recent gas curtailments in Egypt and Trinidad, along with scheduled outages and urea export restrictions in China, have “supported global nitrogen pricing during a period of year that typically sees lower prices and low global shipments as demand shifts from the Northern Hemisphere to the Southern Hemisphere.”

CF said it believes nitrogen channel inventories in North America for all products are below average following strong urea and UAN demand this spring and higher-than-expected planted corn acres. It noted that UAN and ammonia fill programs “achieved prices above 2023 levels despite softening farm economics” due to falling corn and soybean prices.

CF said it believes urea consumption in Brazil in 2024 will be up 3% year-over-year, to more than 8.0 million mt, with urea imports to Brazil in the 7.0-8.0 million mt range this year. It anticipates an active urea import market into India during the second half of the year, with urea exports from China remaining limited.

The company said approximately 25% of ammonia and 30% of urea capacity in Europe was reported in shutdown/curtailment in early July 2024, with operating rates and overall domestic nitrogen product output expected to remain below historical averages over the long term, resulting in higher-than-average imports of ammonia and upgraded products into the region.

CF expects urea and ammonia exports from Russia to increase this year due to the start-up of new urea granular capacity and the completion of the country’s Taman port ammonia terminal in the second half of 2024.

“Over the medium-term, significant energy cost differentials between North American producers and high-cost producers in Europe and Asia are expected to persist,” CF said. “As a result, the company believes the global nitrogen cost curve will remain supportive of strong margin opportunities for low-cost North American producers.”

CF expects the global nitrogen supply-demand balance to tighten over the longer term, however, as global nitrogen capacity growth over the next four years fails to keep pace with expected global nitrogen demand growth of approximately 1.5% per year for traditional applications and new demand growth for clean energy applications.

CF highlighted several low-carbon strategic initiatives, and said it expects “greater clarity later in 2024 regarding demand for low-carbon ammonia, including the ammonia carbon intensity requirements of offtake partners as well as government incentives and regulatory developments in partners’ local jurisdictions.”

Intrepid Potash Inc., Denver, Colo., reported a second-quarter net loss of $0.8 million ($0.06 per diluted share) on total sales of $62.1 million, down from income of $4.3 million ($0.33 per diluted share) and sales of $81 million in last year’s second quarter. Lower sales volumes and net realized prices were cited.

Adjusted EBITDA was $9.2 million for the quarter and $16.9 million for the first six months, down from $15.8 million and $32.2 million, respectively, in 2023. Total revenue came in at $62.05 million for the quarter and $141.3 million for the first six months, down from $81 million and $167.9 million, respectively, in 2023.

Potash and Trio® sales volumes for the quarter were reported at 55,000 st and 63,000 st, respectively, compared with 79,000 st and 63,000 st last year. Average net realized sales prices were $405/st for potash and $314/st for Trio®, down from $479/st and $333/st, respectively, in the second quarter of 2023.

“We sold fewer tons of potash in the second quarter of 2024 compared to the second quarter of 2023, as we had fewer tons of potash to sell due to lower potash production from our HB and Wendover facilities,” Intrepid said, noting the 30% drop in sales volumes and the 15% drop in net realized potash prices.

“Our strategic focus continues to be improving our potash production, and I’m happy to share that we saw the first indications of this in our second-quarter results,” said Matt Preston, Intrepid’s Chief Financial Officer and Acting Principal Executive Officer. “Improved brine grades at HB from the Eddy Cavern and good early-season evaporation rates allowed us to extend our spring production season, and we still expect our 2024 potash production to be approximately 15% higher than 2023.”

“As the broader potash market looks to be finding its midcycle pricing floor, we remain focused on improving our unit economics by means of higher potash production,” Preston added.

Trio® segment sales were down 8% from last year while Trio® sales volumes were flat year-over-year. Intrepid said improved potassium fertilizer supplies pressured Trio® prices, though cost of goods sold were down 18% in the quarter due to improved production rates and decreased total production costs. The company said it produced 68,000 st of Trio® during the quarter, up from 58,000 st last year.

“In Trio®, our sales volumes and production are well ahead of last year’s pace through the first six months of the year as increased operating rates from our new continuous miners and our modified operating schedule have driven significant improvement in both our total and per ton production costs,” Preston said. “Trio® segment gross margin of $2.2 million in the second quarter was an increase of approximately $3.3 million sequentially and $1 million year-over-year.”

Sales in the company’s oilfield solutions segment increased $0.4 million from last year, primarily due to a $0.2 million increase in brine water sales and a $0.3 million increase in other oilfield solution products and services. Intrepid noted increased water and brine water sales due to continued strong demand from oil and gas operators in the Permian Basin near Intrepid South.

As for operational updates, Intrepid said it completed a new extraction well project at is HB Solar Solution Mine in Carlsbad, N.M., in June, and the company expects to commission Phase Two upgrades at the mine in the third quarter, which includes an in-line pigging system to remove scaling and help ensure more consistent flow rates.

A new primary pond at the company’s Wendover, Utah, mine is expected to increase the brine evaporation area and improve production by the fall of 2025, and Intrepid said it continues to advance its lithium project at Wendover.

The company also said it now has all permits to begin construction and operation of its sand project at Intrepid South, but developments there have been paused due to “softening conditions in the oilfield services market.”

Gross margins for the quarter slipped to $7.6 million from $15.4 million, while cash flow from operations dipped to $27.7 million from $30.5 million. Capital expenditures were $11.3 million for the second quarter and $23.0 million for the first six months ended June 30, 2024. The company said it continues to expect full-year 2024 capital expenditures of $40-$50 million.

AdvanSix posted second-quarter net income of $38.9 million on sales of $453.5 million, up from the year-ago $32.7 million and $427.9 million, respectively, citing a 5% increase in sales volume and a 1% increase in net pricing driven by higher sales of nylon and ammonium sulfate amid favorable North American supply and demand conditions. Adjusted EBITDA for the quarter was $78.1 million, up from $65.8 million.

“Our strong second-quarter results, featuring top and bottom line growth as well as year-over-year cash flow improvement, reflect our collective organization’s execution and the advantages of our business model and diverse product portfolio,” said Erin Kane, President and CEO of AdvanSix. “We realized a 6% improvement in sales reflecting higher domestic nylon sales volume, a robust domestic application season for ammonium sulfate, and continued strength in acetone pricing.”

Kane said the company delivered its “second-highest quarter of granular ammonium sulfate production ever” as plant output returned to targeted utilization rates after a first-quarter operational disruption (GM Jan. 19, p. 1). Second-quarter ammonium sulfate sales were $139.7 million, representing 31% of total company sales, versus the year-ago $138.9 million, or 32%.

AdvanSix said it anticipates higher ammonium sulfate pricing in the third quarter compared with last year, reflecting robust demand entering fall fill, though it noted that “typical North American ammonium sulfate seasonality” is expected to drive sequential pricing declines in the third quarter.

“While we anticipate typical North American ammonium sulfate seasonality, we are starting the third quarter with a strong fall fill program at higher pricing levels compared to the prior year,” Kane said. “Over the long-term, we continue to positively position the enterprise through high-return growth and cost savings programs, an improved portfolio mix, and disciplined capital deployment to fuel future earnings, cash flow performance and robust total shareholder returns.”

Cash flow from operations was reported at $50.2 million for the quarter, up $15.2 million from last year due to higher net income the favorable impact of changes in working capital, while capital expenditures were up $14.2 million, to $33.5 million, primarily due to maintenance and enterprise programs.

AdvanSix continues to expect capital expenditures of $140-$150 million in 2024 to address critical enterprise risk mitigation and growth projects, including the company’s SUSTAIN (Sustainable U.S. Sulfate to Accelerate Increased Nutrition) program. The company anticipates a pre-tax income impact of $38-$43 million in 2024 due to planned plant turnarounds.

The company’s Board of Directors declared a quarterly cash dividend of $0.16 per share on the company’s common stock, payable on Aug. 27, 2024, to stockholders of record as of the close of business on Aug. 13, 2024.

Nutrien Ltd. on Aug. 7 announced the appointment of Mark Thompson as Executive Vice President and Chief Financial Officer, effective Aug. 26, 2024. Thompson succeeds Pedro Farah, who will remain with Nutrien in an advisory capacity until his departure on Dec.31, 2024.

Thompson currently serves as Executive Vice President and Chief Commercial Officer, and has been with Nutrien since 2011. He previously held numerous executive and senior leadership roles across the company, including Chief Strategy & Sustainability Officer, Chief Corporate Development & Strategy Officer, and Vice President of Business Development for Nutrien’s Retail business.

“Mark’s impressive track record of execution, along with his proven financial and strategic acumen provides the unique ability to succeed in this position on day one. He brings in-depth knowledge of our business that will support the advancement of our strategic actions to enhance quality of earnings and cash flow,” said Ken Seitz, Nutrien President and CEO. “On behalf of the Nutrien team, I would also like to thank Pedro for his service and commitment to Nutrien over the last five years.”