| 11/4/2022 | Last Week | |

| Memphis | 16.00 | 16.00 |

| St. Louis | 17.00 | 17.00 |

| Peoria | 22.00-23.00 | 22.00-23.00 |

| Cincinnati | 26.00 | 26.00 |

| St. Paul | 28.00 | 28.00 |

| Catoosa/Inola | 31.00-32.00 | 31.00-32.00 |

All posts by jlarareo@bloomberg.net

Data Signals

Fertilizer Futures

Dry Fertilizer Barge Rates

| 10/28/2022 | Last Week | |

| Memphis | 16.00 | 16.00 |

| St. Louis | 17.00 | 17.00 |

| Peoria | 22.00-23.00 | 22.00-23.00 |

| Cincinnati | 26.00 | 26.00 |

| St. Paul | 28.00 | 28.00 |

| Catoosa/Inola | 31.00-32.00 | 31.00-32.00 |

Data Signals

Ammonia

US Gulf/Tampa:

Tampa ammonia for October continues to stand at $1,175/mt CFR, up $25/mt from September’s $1,150/mt CFR. With lower natural gas prices in Europe and more ammonia plants coming back up, Tampa prices could be under more pressure for November.

Eastern Cornbelt:

Fall ammonia application was underway in Illinois, although activity was spotty. The Eastern Cornbelt market remained at $1,300- $1,400/st FOB for available offers, with the low confirmed at Lima, Ohio, and the high at East Dubuque, Ill.

Although many locations were not quoting prices at mid-month, sources said $1,350/st FOB deals could likely be had at Huntington and Mount Vernon, Ind.

Western Cornbelt:

The ammonia market in the Western Cornbelt was reported in the $1,250-$1,300/st FOB range, with the low in Nebraska and the high in Missouri. Pricing in the Southern Plains remained at $1,100/st FOB Woodward, Okla., $1,150/st FOB Verdigris, Okla., and $1,175/st FOB Coffeyville, Kan.

California:

Anhydrous ammonia pricing in California was steady at $1,250/st DEL. The aqua ammonia remained at $271-$336/st FOB, with the low reported for the last offers at Stockton and the high at Sycamore.

Pacific Northwest:

Ammonia pricing in the Pacific Northwest was pegged at $1,325/st FOB and $1,350/st DEL at mid-month. The aqua ammonia market remained at $345/st FOB in the region.

Western Canada:

The last prices for ammonia remained at C$1,600-$1,800/mt DEL for fall tons in the region, but most offers were pulled by mid-October.

India:

Sources said demand for ammonia should be picking up along with an expected increase in domestic DAP production. For now, ammonia prices remain stable at $850-$900/mt CFR.

The latest numbers released by the Indian government show January-August 2022 imports at 1.4 million mt, according to Trade Data Monitor, down roughly 12% from the 1.6 million mt imported during the same period in 2021.

The main suppliers to India for the first eight months of the year were Saudi Arabi with 621,000 mt, Qatar with 257,000 mt, Bahrain with 159,000 mt, and Indonesia with 129,000 mt.

August 2022 imports were reported at 226,000 mt, up 10% from the 205,000 mt imported during August 2021. Saudi Arabia accounted for 47% of the total imports in August 2022 with 105,000 mt. Bahrain took 18% of the market with 42,000 mt, and Indonesia another 12% with 28,000 mt.

Middle East:

Arab Gulf producers are mostly satisfied with their contract orders. Spot buyers are being hit with prices at $1,100/mt FOB and up. Sources said this level is too high to match the landed prices around the world. Traders said the real spot price – if one existed – should be no higher than $1,050/mt FOB.

Contracts sales are reportedly being shipped out at $1,000/mt FOB. Sources said this level matches up with the Northwest Europe price, but is still too high for Indian and Southeast Asian buyers.

Iranian ammonia exports for January-September 2022 were reported at 361,000 mt by Trade Data Monitor, down 20% from the 449,000 mt exported during the same period in 2021. India dominated the Iranian order books with 302,000 mt.Third-quarter exports were reported at 119,000 mt, down from 132,000 mt last year.

September 2022 exports were pegged at 25,000 mt, down from 35,000 mt in September 2021. India took 53% of the Septembers orders with 18,500 mt, and Oman purchased 14,000 mt for 39% of the export market from Iran. Sources said some of the material shipped to Oman was “nationalized” before being shipped onward to other buyers.

Northwest Europe:

Ammonia prices have settled at $1,250/mt CFR. Material is available at workable prices from Trinidad to Indonesia. Buyers are rejecting offers of $1,100/mt FOB from the Arab Gulf, as well as the tonnage produced in Europe, which is beyond market levels because of the high price of natural gas.

Southeast Asia:

Ammonia demand in the region remains soft as buyers continue to look for ways to limit their contractual requirements. The main suppliers in the area – Indonesia and Malaysia – continue to sell more of their product to buyers in Europe and India. Even more Chinese ammonia is finding its way West.

South Korean ammonia imports for January-September 2022 were reported at 1 million mt by Trade Data Monitor, down about 8% from the 1.1 million mt imported during the same period in 2021. The main suppliers so far have been Indonesia with 473,000 mt, and Saudi Arabia with 427,000 mt.

Third-quarter imports into South Korea were reported at 328,000 mt, down from the 384,000 mt imported during the same quarter in 2021.

September 2022 imports were reported at 78,000 mt, down about a third from the 116,000 mt imported during September 2021. Suppliers were Saudi Arabia with 40,000 mt for 52% of the import market, followed by Indonesia with 23,000 mt for 29% of the imports. Bahrain also added 10,000 mt for 12% of the market.

Urea

US Gulf:

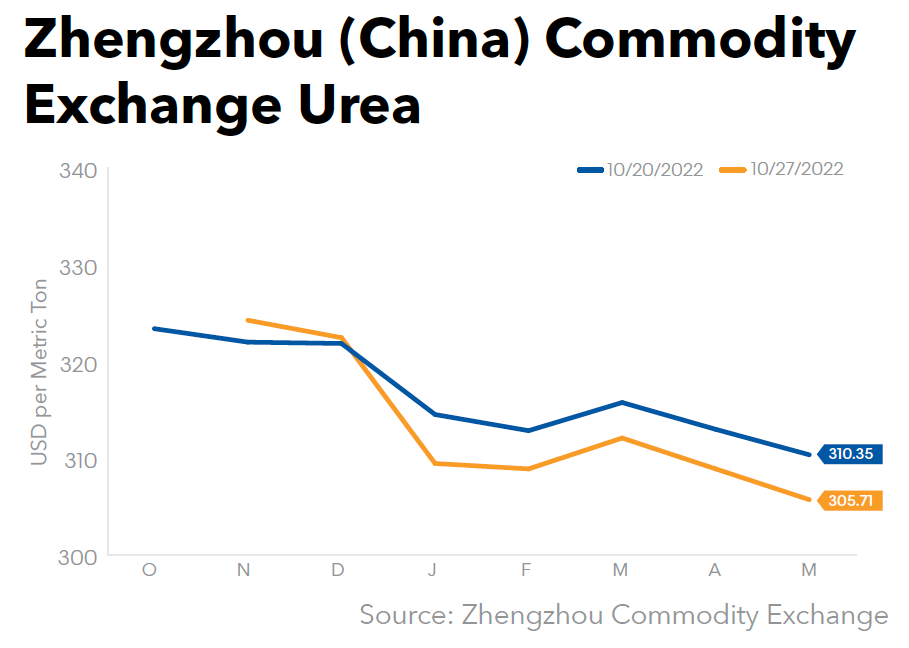

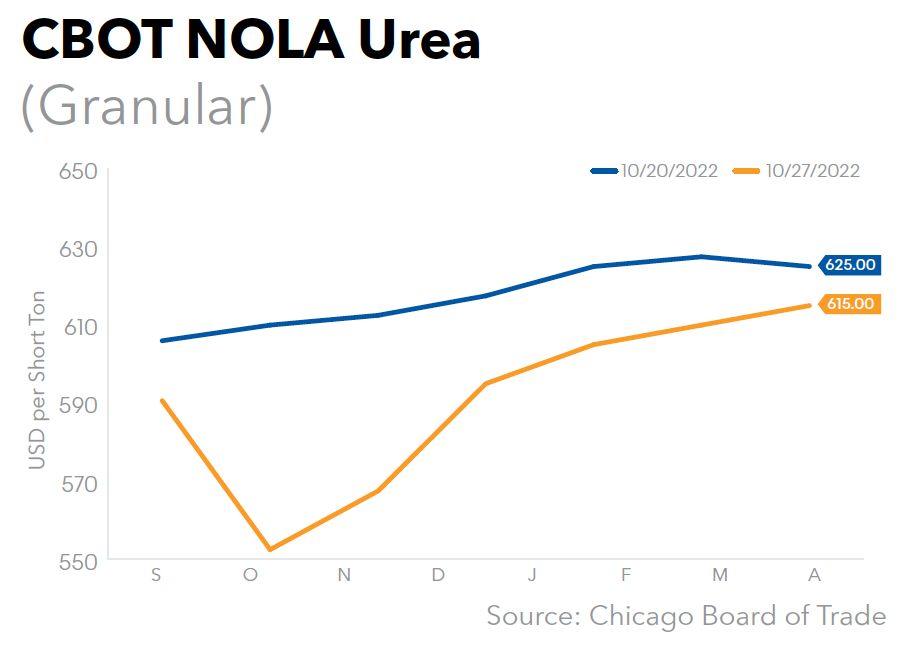

NOLA urea barges were quoted at $580-$600/st FOB, down from the week-ago $595-$615/st FOB.

Eastern Cornbelt:

Urea terminal prices fell to $660-$690/st FOB in the Eastern Cornbelt, with the low reported at Cincinnati, Ohio.

Western Cornbelt:

Urea pricing was reported in a broad range at $660-$690/st FOB in the Western Cornbelt, depending on location, with the low confirmed at St. Louis, Mo., and the high in Iowa.

In the Northern Plains, delivered urea reportedly fell to $685-$750/st in North Dakota, with the low for railed tons from Canada and the high for truck-DEL material.

California:

Urea pricing in California was pegged at $760-$780/st FOB Stockton at midweek, down from a high of $840/st in late September. Reference pricing for 50 pound bags remained at the $900/st level FOB Stockton.

Pacific Northwest:

The urea market was pegged at $735-$750/st FOB in the Pacific Northwest, with the low confirmed at Rivergate, Ore. Rail-DEL urea pricing was pegged in the $720-$732/st range in mid-October, with truck-DEL tons reported at $730-$750/st in Montana.

Western Canada:

Urea prices were reported in a broad range at C$1,085-$1,135/mt FOB in Western Canada, up C$15/mt at the high, while the delivered market was pegged at C$1,110-$1,130/mt in the region in mid-October.

India:

The IPL urea tender closed on Oct. 17 with 19 companies offering 2.7 million mt. The lowest offers were from Ameropa with 141,450 mt at $649.48/mt CFR for West Coast ports, and from AgriCommodities with 72,500 mt at $655/mt CFR for East Coast deliveries. No producers offered directly into the tender.

Going into the tender, sources were expecting to see prices soften from the $668-$675/mt CFR achieved in the previous tender. Most were satisfied the current price does not represent a crash, but rather a predicable correction in pricing.

| Offering Company | Quantity (MT) | US$/mt CFR | Discharge Port |

| Ameropa | 141,450 | 649.48 | WCI-L1 |

| 141,450 | 659.67 | ECI | |

| AgriCommodities | 72,500 | 655.00 | ECI-L1 |

| 77,500 | 680.40 | WCI | |

| Alkagesta | 25,000 | 689.00 | WCI |

| Aakra Dubai | 50,000 | 668.00 | WCI |

| Aries | 100,000 | 666.79 | ECI |

| Continental | 90,000 | 656.00 | WCI |

| 90,000 | 659.00 | ECI | |

| Dreymoor | 75,000 | 680.00 | WCI |

| 42,000 | 695.00 | ECI | |

| Fertcom | 45,000 | 668.50 | WCI |

| 45,000 | 705.00 | ECI | |

| Fertiglobe | 45,000 | 652.00 | WCI |

| Gavilon/MacroSource | 45,000 | 657.50 | ECI |

| Keytrade | 60,000 | 680.00 | ECI |

| Koch | 77,000 | 660.00 | WCI |

| 670.00 | ECI | ||

| Midgulf | 105,000 | 672.00 | WCI |

| 105,000 | 675.00 | ECI | |

| OQ Trading | 147,500 | 654.00 | WCI |

| 148,500 | 656.50 | ECI | |

| Sabic | 175,000 | 670.00 | WCI |

| Samsung | 180,000 | 649.70 | WCI |

| 125,000 | 657.00 | ECI | |

| Southern Cross | 50,000 | 703.00 | WCI |

| Sun International | 45,000 | 670.00 | WCI |

| Swiss Singapore | 250,000 | 650.00 | WCI |

| 150,000 | 655.50 | ECI |

Sources said IPL initially targeted getting 1.5 million mt, but traders said the buyer could most likely take closer to 2 million mt. The buyer issued counterbids to the six companies with offers just after the Ameropa and AgriCommodities prices for each coast. As Green Markets went to press, IPL had awarded nearly 1 million mt from this round of counterbids.

The total awarded tonnage of 997,500 mt includes the 141,450 mt from Ameropa and the 72,500 mt that was automatically awarded because they had the lowest offers.

| Offering Company | Awarded Quantity (mt) |

| OC Trading | 296,000 |

| Ameropa | 189,000 |

| Swiss Singapore | 180,000 |

| Samsung | 170,000 |

| AgriCommodities | 72,500 |

| Gavilon/MarcoSource | 45,000 |

| Fertiglobe | 45,000 |

IPL has reportedly moved on to the rest of the offering companies to secure more product. The companies have to respond by Oct. 21. As noted previously, sources are confident IPL should be able to get closer to 2 million mt. Traders had noted earlier that if IPL fails to take 1.5 million mt, the market could face further price softening. Failure to take 1 million mt could lead to a price crash, said sources.

Reportedly issues affecting offers into this tender went beyond the Chinese export restrictions and the limited availability from Russia. Sources said suppliers from Vietnam did not want to participate because of the expectation of softer prices. Indonesian suppliers also stepped back after they figured the drop in pricing would not be as precipitous as earlier expectations.

Sources said some traders also held long positions that they had to move, which prompted some to worry about a more severe price drop.

High gas prices in Europe are also causing European buyers to be anxious. Because of the gas prices, producing urea in Europe is more expensive than importing. The North African urea producers have appeared to remain fixated on Europe, leaving fewer – if any – tons for offers into India.

Sources said even if IPL takes 2 million mt, India will still need another tender before the end of the year to fill out its anticipated needs for this season. The most likely call for the tender would come close to the Dec. 5 shipping deadline from the IPL tender.

January-August 2022 urea imports in India totaled 6.2 million mt, according to Trade Data Monitor, up about a third from the 4.7 million mt imported during the same period in 2021. Total sales into India from the Arab Gulf were reported at 2.6 million mt. China, formerly a major exporter to India, shipped 699,000 mt.

August 2022 imports were reported at 492,000 mt, down 57% from the 1.2 million mt imported during August 2021. The need to pull urea from multiple locations was evident in the source countries during August. Sources said the material designated from Finland is most likely re-exported Russian urea.

| Source Country | Quantity (mt |

| Qatar | 126,000 |

| Oman | 118,000 |

| Indonesia | 73,000 |

| Finland | 51,000 |

| United States | 49,000 |

| Bahrain | 47,000 |

Pakistan:

The Oct. 17 tender for 300,000 mt called by TCP was scrapped after only one company offered material. The buying house found irregularities in that company’s paperwork, forcing it to be disqualified.

A follow-up tender was called on Oct. 19 for the same amount to close on Oct. 26. Shipment of the material is to be broken into three tranches of 100,000 mt each, with arrival dates of Nov. 7-13, Nov. 15-22, and Nov. 25–Dec. 1.

Industry sources continue to have concerns about some of the financing protocols in the tender, as well as the ability of TCP to pay on time. Sources pointed to delays in payments for previous wheat purchases and the scrapping of a recent wheat purchase tender.

Traders are careful to point out that while some of the wheat deals were paid late, they were eventually paid. So far, said one trader, Pakistan has not defaulted on any of its purchases despite its limited foreign cash reserves.

Indonesia:

Sources said Kaltim scrapped its most recent auction. Swiss Singapore was the highest bidder at $571/mt FOB. Sources said once it was clear the price in the Indian tender would not crash, the Indonesian producers pulled back, most likely in the hopes of achieving a higher level.

A new selling tender is expected as early as Oct. 21. One trader said granular prices should end up being much higher during the IPL tender shipping period.

Middle East:

The netback to the Arab Gulf from the IPL tender was put in the mid-$620s/mt FOB. The price is lower than previous business, said one trader, but not dramatically so.

Producers from the area did not offer directly into the IPL tender. This led sources to speculate that traders will receive sufficient support in the tender to fill the producers’ order books and to supply India with the tonnage they need.

Egyptian producers remained quiet during the week. Sources said they will most likely remain focused on their European and African buyers rather than drop prices to meet the Indian tender price. The last done business out of Egypt was $760/mt FOB to a trader for Europe. To meet the Indian price, the producers would have to accept a netback closer to $600/mt FOB.

Sources said because of the high cost to produce urea in Europe, buyers there are keeping a close eye on prices and supplies out of Northern Africa and Egypt. So far, importing urea has remained cheaper than producing in Europe.

Iranian exports of urea have picked up. January-September 2022 exports were reported at 3.7 million mt by Trade Data Monitor, up about a quarter from the 2.9 million mt exported during the same period in 2021. Turkey was the single largest buyer, taking 1.2 million mt. South Africa with 427,000 mt and Mozambique with 304,000 mt followed.

Major urea producer Nigeria also took 259,000 mt. Sources have speculated that these purchases by Nigeria might be used for their own market, freeing up more Nigerian urea for export.

Third-quarter exports were reported at 1.5 million mt, up 12% from the 1.2 million mt exported during the same period last year.

September 2022 exports were up dramatically, to 541,000 mt from the 401,000 mt exported during September 2021. Turkey was responsible for buying 47% of exports with 254,000 mt. Mozambique took 76,000 mt for 14% of the market, while Nigeria and Sudan each took 65,000 mt for 12% each of the export market.

China:

The netback to China from the IPL/India tender is reported in the upper-$620s/mt FOB. Sources said there is enough material in the portside warehouses to cover potential awards of Chinese product. Additional tons are also likely to be made available during the shipping period up to Dec. 5, if necessary.

Traders are still hesitant to take any forward positions with Chinese product. Sources noted disruptions in production could occur because of the strict COVID policies imposed by Beijing. They also worry that customs officials could delay the export of a cargo by slowing down the paperwork process.

South Korea:

January-September 2022 imports of urea were reported at 754,000 mt by Trade Data Monitor, up about 7% from the 703,000 mt imported during the same period in 2021. South Korean buyers reached out to a number of suppliers. While Chinese suppliers were the single largest source with 295,000 mt, other suppliers included Qatar with 183,000 mt, and Indonesia with 90,000 mt.

Third-quarter imports were reported at 193,000 mt, down almost 30% from the 214,000 mt imported during the same period last year. September imports were reported at 40,000 mt, down more than half from the 84,000 mt imported during September 2021.

Brazil:

Urea prices slipped to $650-$670/mt CFR, with buyers pushing for even further discounts. Sources said new bids are coming in at $610-$630/mt CFR, but with no takers yet. The low bid prices are reportedly being actively discussed for material from sanctioned counties such as Venezuela and Iran.

Buyers are watching India and Nigeria closely for a potential turnaround in pricing. Sources are concerned that if India takes the 2 million mt expected by international traders, it could tighten the urea market enough to push up prices into Brazil. In addition, flooding in Nigeria has reportedly affected production at Indorama.

Nigeria has grown into a major supplier for Brazil. About 18% of urea imports so far this year have come from Nigeria, compared with 8% in 2021 for the same period.

Rondonopolis urea pricing is reported up at $800-$845/mt FOB ex-warehouse. Some of the disconnect from lower port prices appears to come from a lack of clarity about what will happen to exchange rates and government policy towards farmers following the Oct. 30 presidential election.

UAN

US Gulf:

NOLA UAN barge prices remained in the $550-$555/st ($17.19-17.34/unit) FOB range.

Eastern Cornbelt:

UAN-32 in the Eastern Cornbelt remained at $595-$620/st ($18.59-$19.38/unit) FOB, depending on location and availability, with rail-DEL pricing in the $625-$635/st ($19.53-$19.84/unit) range in the region. The last UAN-28 offers were quoted at $530/st ($18.93/unit) FOB Cincinnati.

“4Q offers out of river terminals are getting harder to find as water levels impede barge movement,” commented one source.

Western Cornbelt:

UAN-32 prices in the Western Cornbelt were steady at $585-$610/st ($18.28-$19.06/unit) FOB for limited offers, with the low confirmed at Port Neal, Iowa, and the high at Muscatine, Iowa. The St. Louis market remained at $590-$600/st ($18.43-$18.75/unit) FOB for the last offers.

Rail-DEL pricing was pegged at the $615/st ($19.22/unit) level or higher in the region.

California:

UAN-32 prices were quoted in a broad range at $590-$630/st ($18.44-$19.69/unit) FOB Stockton, with the high reflecting a $30/st increase from last report. New postings at other locations included $635/st ($19.84/unit) FOB Port Hueneme and $640/st ($20.00/unit) FOB West Sacramento.

Pacific Northwest:

The UAN-32 market covered a wide range at $610-$670/st ($19.06-$20.94/unit) FOB in the Pacific Northwest, depending on location and supplier, with the high confirmed at midweek for new offers out of spot truck terminals. Prices at Kennewick, Wash., were confirmed at the $650/st ($20.31/unit) FOB level. Delivered pricing in the region was reported in the $655-$680/st ($20.47-$21.25/unit) range at mid-month.

Western Canada:

The UAN-28 market in Western Canada was reported at C$715-$725/mt (C$25.54-$25.89/unit) DEL for October-December tons, down C$15/mt at the high end of the range.

Ammonium Nitrate

Western Cornbelt:

The ammonium nitrate market was unchanged at $640-$650/st FOB Missouri terminals for the last reported offers.

Ammonium Sulfate

US Gulf:

NOLA ammonium sulfate barges continued to be quoted in the $400-$410/st FOB range.

Eastern Cornbelt:

The granular ammonium sulfate market remained at $460-$480/st FOB in the Eastern Cornbelt, depending on location, with the Cincinnati market quoted in the $465-$480/st FOB range at mid-month.

In the Eastern US, AdvanSix on Oct. 17 raised its ammonium sulfate postings at Hopewell, Va., to $490/st FOB for granular, $450/st FOB for mid-grade, and $430/st FOB for standard. Those levels are up $40/st from the company’s Aug. 15 reference prices.

Western Cornbelt:

Granular ammonium sulfate pricing was quoted at $445-$480/st FOB in the Western Cornbelt, with the low confirmed at St. Louis and the high in Iowa.

California:

The granular ammonium sulfate market was quoted at $525-$570/st FOB in California, depending on grade and location, with the low reflecting offers at Lathrop, Woodland, and Richvale.

Pacific Northwest:

Granular ammonium sulfate remained at $470-$490/st FOB or DEL in the Pacific Northwest. Standard grade was reported at $420/st FOB and $420-$445/st DEL, depending on location.

IRM’s Oct. 4 postings for ammonium sulfate FOB warehouses or DEL in Washington, Oregon, Utah, Idaho, and Montana included $470/st for Transzform and WesternPremium, and $420/st for WesternStandard. The WesternStandard posting reflects a $20/st increase from the last reference prices.

Western Canada:

Ammonium sulfate prices in Western Canada were pegged at C$665-$680/mt DEL for fall tons, with postings remaining as high as C$735/mt DEL from some suppliers.

China:

Prices in China remain stagnant at $220-$225/mt FOB for caprolactam-grade amsul. Sources said most of the deals are taking place at the lower end of the range.

Brazil:

The landed ammonium sulfate price remains at $280-$295/mt CFR, with the bulk of the business taking place in the $280s/mt CFR. Sources said there is a push for higher levels, with some future pricing looking at $290-$295/mt CFR.

The anticipation of higher amsul prices comes as buyers look to possible urea price increases as the year winds down and the next season begins to kick into gear. There is also concern that with India looking to take 2 million mt of urea in its tender, the market could tighten and force up the ammonium sulfate price.

Rondonopolis prices moved up to $420/mt FOB ex-warehouse.

South Korea:

Ammonium sulfate exports from South Korea dropped to 191,000 mt for January-September 2022, according to Trade Data Monitor, down 58% from the 454,000 mt exported during the same period in 2021. The main buyers were Mexico with 83,000 mt, the US with 59,000 mt, and New Zealand with 41,000 mt.

Third-quarter 2022 sales of 65,000 mt were off by about a half from the 133,000 mt exported during the same quarter of 2021.

September 2022 sales were limited to 364 mt, down from 72,000 mt exported during September 2021 and 45,000 mt in September 2020. The low amount is unusual, but not unprecedented. May 2022 exports were at 142 mt and January 2022 showed exports of 6,000 mt. The rest of the months of the year had exports ranging from 15,000-60,000 mt.