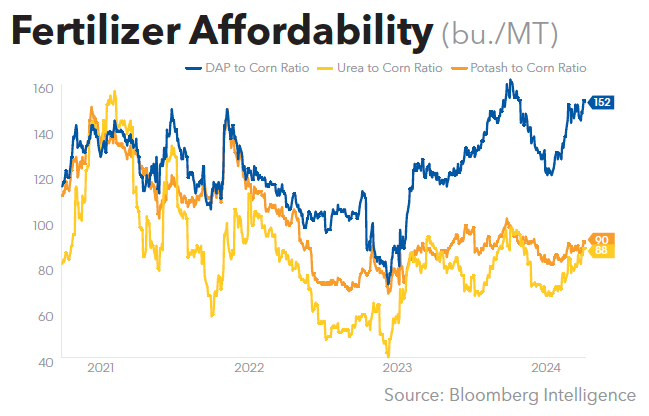

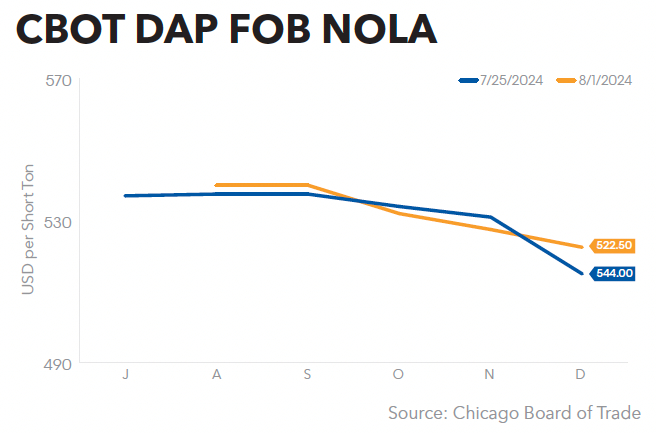

Fertilizer Futures

The CEO of Canadian Pacific Kansas City Ltd. (CPKC) railway said a strike by the Teamsters Canada Rail Conference (TCRC) now seems likely in the second half of August, according to multiple media reports.

TCRC represents nearly 10,000 conductors, locomotive engineers, and yard workers at Canadian National (CN) and CPKC, including 3,300 at CPKC alone. CPKC CEO Keith Creel told analysts on a July 30 conference call that the railroads and union remain “fair apart” on negotiations over a new collective agreement.

“I’m just being transparent and honest. It’s going to be a challenge,” Creel said. “We’re going to remain cautiously optimistic. But we’re not going to do a bad deal, either.”

The railroads and TCRC are still awaiting a decision by the Canadian Industrial Relations Board (CIRB), which is considering whether a strike would compromise safety and essential services. CIRB in July said it expects to make its ruling by Aug. 9 (GM July 19, p. 1), and no strike or lockout can take place until at least 72 hours after the decision.

“You can imagine the impact, obviously, of most railroads in the nation being shut down,” Creel said, warning of “mass chaos” if the railway can’t alert their clients to a work stoppage several weeks in advance.

Creel noted that revenues from container traffic fell 4% year-over-year as customers rerouted some shipments due to strike concerns, but said a labor disruption will not affect CPKC’s financial guidance so long as it lasts less than two weeks, the Canadian Press reported. Last week, CN lowered its forecast for earnings growth amid fallout from the strike threat as clients seek to steer clear of Canadian ports and rail lines.

“It’s impacting our business, particularly in the international intermodal where customers have taken actions to reroute vessels away from Canadian ports until the labor questions have been resolved,” said CN CEO Tracy Robinson in a July earnings call. Intermodal volume dropped 17% from May 12 to July 14, according to CN.

According to Trains magazine, a strike would shut down both CPKC and CN in Canada, and would also affect commuter operations in Vancouver, Toronto, and Montreal because the trains operate on trackage dispatched by CPKC rail traffic controllers, who are represented by the TCRC.

ICL Group Ltd. on July 29 announced that it has acquired Custom Ag Formulators (CAF), a North American provider of customized agriculture formulations and products for growers. The acquisition for approximately $60 million is part of ICL’s effort to expand its Growing Solutions product offering and to position the business for further growth in new and adjacent end-markets.

“We are pleased to have Custom Ag Formulators join ICL and bring their expertise to our customers in the US,” said Elad Aharonson, President of ICL Growing Solutions. “This acquisition helps further the growth of our global Growing Solutions business, by enabling us to meet the distinctive needs of local growers through our existing distribution partners. It also allows us to address the specific requirements of farmers across the growing regions of the West Coast and the Southeast, where crops – and their nutritional needs – can vary greatly.”

CAF operates two manufacturing sites, one in Fresno, Calif., and the other in Adel, Ga., where the company produces liquid and dry adjuvants and enhanced nutrients, as well as various other specialty products, in customized agricultural formulations and packaging. CAF’s strategic locations allow it to ship same-day to growing regions on both the US East and West Coasts, as well as to the central US.

“Custom Ag Formulators was founded to provide quality products with custom formulations and packaging in a timely and efficient manner,” said Patrick Murray, CAF Principal and Director of Sales. “For more than 25 years, our mission has been to consistently lead the industry in customer service, quality, and product innovation, and we are excited to move this mission forward with ICL Group.”

This is the second Growing Solutions acquisition for ICL in 2024. The first, completed earlier this year, was the $30 million purchase of Nitro 1000, a manufacturer, developer, and provider of biological crop inputs in Brazil (GM March 1, p. 30).

Yara International ASA reported second-quarter EBITDA excluding special itemsof $513 million on improved margins, compared with $252 million in second-quarter 2023 and beating the average analyst estimate of $462 million. Net income for the quarter was $3 million on revenues of $3.53 billion, compared with a net loss of $298 million last year.

Yara said the global nitrogen market tightened during second quarter, due to the absence of Chinese exports and supply restrictions in Egypt.

“I’m pleased to see improved results, with higher margins and deliveries in a more stable price environment,” said Svein Tore Holsether, President and CEO. “However, returns are not at satisfactory levels. We have been through turbulent, volatile years which Yara has navigated well, but we now need to adjust our priorities and cost base, to improve Yara’s profitability.”

To that end, Yara said it has initiated a cost and capex reduction program to strengthen its financial performance and improve shareholder returns going forward. The Oslo-based company plans to cut fixed costs and capital expenditure by $150 million each by the end of 2025 by prioritizing high-return core business and scaling down tail-return activities.

Yara said that a final investment decision for its US clean ammonia investments is still planned for the second half of 2025, provided projects “are set for strong double-digit returns.” Sound funding and risk-adjusted project returns above 10% are key requirements for all growth projects, the company noted.

“Yara has unique competitive edges as an integrated nitrogen producer with a global asset footprint and downstream presence,” Holsether said. “This gives us scale, flexibility and optionality in how we optimize our business, including our ammonia production and trade, and it positions Yara well for profitable decarbonization. With a sharpened strategic focus and growing demand for low-carbon crop solutions, Yara is set to increase value creation and shareholder returns going forward.”

Yara shares rose as much as 4.1% after the earnings release, the most since Feb. 9, but have declined about 19% over the past year, with subdued fertilizer demand and uncertainty over how the company will raise funds for its clean ammonia plans weighing on the stock.

“Yara’s $300 million plan to trim costs and reduce capital spending aims to boost return on invested capital metrics by 2%, bringing it closer to its target of 10% in the next 18 months,” said Bloomberg Intelligence Analyst and Green Markets Research Director Alexis Maxwell. “The company sees $150 million in fixed-cost savings and the rest coming from capex, which falls to $1.2 billion in 2024.”

CVR Energy Inc., Sugar Land, Texas, on July 29 announced second-quarter net income attributable to CVR Energy stockholders of $21 million (21 cents per diluted share) and EBITDA of $103 million, down from $130 million ($1.29 per diluted share) and $300 million, respectively, in last year’s second quarter.

Net sales for the second quarter came in at $1.97 billion, beating the average analyst estimate (Bloomberg Consensus) of $1.78 billion. Adjusted earnings per diluted share was 9 cents and adjusted EBITDA was $87 million, compared with $1.64 and $347 million, respectively, last year and up from the average analyst estimate (Bloomberg Consensus) of $80 million.

The second quarter earnings results were attributed to lower refining margins due to a decrease in the Group 3 2-1-1 crack spread and reduced throughputs related to a fire at the company’s 78,000 b/d Wynnewood, Okla., refinery that occurred during severe weather in late April, said Dave Lamp, CVR Energy’s CEO. The refinery is now operating at normal rates.

Net income from CVR’s petroleum operations fell to $18 million from $194 million in last year’s second quarter, with Lamp citing weakness in the Midcontinent refined product market as well as downtime and higher expenses related to the Wynnewood fire.

The Nitrogen Fertilizer Segment reported second-quarter net income of $26 million and EBITDA of $54 million on net sales of $133 million, down from last year’s net income of $60 million and EBITDA of $87 million on net sales of $183 million. Nitrogen fertilizer net sales came in at $133 million, beating the average analyst estimate of $115.9 million.

Production at the CVR Partners LP’s fertilizer facilities remained consistent compared to the second quarter of 2023, producing a combined 221,000 st of ammonia during the second quarter, of which 69,000 st were available for sale while the rest was upgraded to other fertilizer products, including 337,000 st of UAN.

Last year’s second quarter saw combined production of 219,000 st of ammonia, with 70,000 st available for sale and the rest upgraded, including 339,000 st of UAN. Average second-quarter realized gate prices for UAN were down 15% from last year, to $268/st from $316/st, while ammonia was down 26%, to $520/st from $707/st.

“CVR Partners achieved solid operating results for the second quarter of 2024 driven by a combined ammonia production rate of 102%,” Lamp said. He added that CVR continues “to explore strategic transactions both in refining and potentially related to the CVR Partners, although we have nothing to report at this point.”

Consolidated cash and cash equivalents were $586 million as of June 30, an increase of $5 million from Dec. 31, 2023. Consolidated total debt and finance lease obligations were $1.6 billion as of June 30, including $548 million held by the Nitrogen Fertilizer Segment.

CVR Energy announced a second-quarter cash dividend of 50 cents per share, while CVR Partners declared a second-quarter cash distribution of $1.90 per common unit. Both will be paid on Aug. 19, 2024, to common unitholders of record as of Aug. 12, 2024.

LSB Industries Inc., Oklahoma City, Okla., on July 31 reported net income of $10 million on net sales of $140 million for the second quarter ended June 30, 2024, down from $25 million and $166 million, respectively, in last year’s second quarter.

Second quarter adjusted EBITDA was reported at $41 million, down from $47 million last year, while diluted earnings per share came in at $0.13, compared with $0.33 in second-quarter 2023.

“Our second quarter profitability improved sequentially due largely to improved pricing relative to the first quarter of this year,” said LSB President and CEO Mark Behrman. “While selling prices were down compared to the second quarter of last year, the year-over-year pricing decline was much less significant than the declines experienced over the previous several quarters. We view this as indicative of a stabilization of our markets after a period of downward volatility following the spike in nitrogen prices experienced in 2022.”

LSB described the ammonia market as healthy, with strong pricing driven by a brisk summer fill program, natural gas curtailments in Trinidad and Egypt, extended turnarounds and delayed startup of new capacity, and constrained imports into Europe and the Middle East due to shipping disruptions in the Suez Canal.

The company also noted “solid” UAN pricing following the spring application season, and said its industrial business is seeing steady demand for nitric acid and ammonium nitrate, bolstered by US metals production and infrastructure upgrades and expansion.

Behrman said the company recently started a turnaround at its Pryor, Okla., facility and plans to conduct a turnaround at the Cherokee, Ala., plant in the fourth quarter. “When combined with the multiple smaller projects we have underway, we expect these turnarounds to lead to increased reliability and incremental EBITDA and cash flow,” he said.

LSB noted its five-year agreement with Freeport Minerals Corp., Phoenix, Ariz., to supply up to 150,000 st/y of low carbon ammonium nitrate solution (ANS) from LSB’s El Dorado, Ark., facility, starting in 2025 (GM May 24, p. 1).

“Our second quarter was highlighted by our landmark agreement to supply Freeport Minerals with low carbon ANS for use in their copper mining operations,” Behrman said. “This agreement validates our belief that industrial customers will identify low carbon nitrogen products as a critical pathway toward achieving their decarbonization initiatives.”

Behrman also noted LSB’s progress on two clean ammonia projects at El Dorado and the Houston Ship Channel. The El Dorado project would capture and sequester 400,000-500,000 mt/y of CO2, reducing Scope 1 emissions by 25% and yielding 305,000-380,000 mt/y of low carbon ammonia.

“The EPA is currently indicating a final decision next spring on the Class VI permit application submitted by our partner, Lapis Energy, for our El Dorado carbon capture and sequestration project,” Behrman said. “This timeline would position us to begin producing low carbon ammonia by early 2026.”

LSB’s Houston Ship Channel project with INPEX, Air Liquide, and Vopak Exolum envisions a 1.1 million mt/y blue ammonia plant utilizing blue hydrogen provide by Air Liquide/INPEX (GM Oct. 6, 2023). LSB said the Pre-FEED is underway and expected to be completed in the fourth quarter, with the FEED beginning in the first quarter of 2025. A final investment decision is expected in the first quarter of 2026.

“Concurrently, we continue to have productive conversations with potential off-take parties for the low carbon product from this facility,” Behrman said. “We are encouraged by the positive developments with both of our projects and remain committed to our vision of becoming a leader in the global energy transition through the production of low carbon ammonia and downstream products over the next several years.”

LSB repurchased $64 million in principal amount of Senior Secured Notes and approximately 0.8 million shares of common stock during the second quarter, with year-to-date figures reported at $97 million and 1.5 million, respectively. The company reported total debt of approximately $486 million as of June 30, while cash flow from operations was reported at $41 million and capital expenditures at $15 million.

HNH Energy, a consortium of Austria Energy Group, Copenhagen Infrastructure Partners (CIP), and Ӧkowind, has submitted plans for its green ammonia project to Chile’s Environmental Impact Assessment System in anticipation of starting construction in 2027 with commissioning in 2030. The project involves an estimated investment of $11 billion.

The project will be in San Gregorio in the Magallanes region, which is near the southern tip of Chile. It will produce export-oriented green hydrogen and green ammonia, and will consist of a 1.4 GW onshore wind farm, electrolyzers, ammonia plant, port facility, and seawater desalination plant. It is expected to produce 1.3 million mt/y of green ammonia and 270,000 mt/y of hydrogen, with development occurring in two stages due to land occupation uncertainties.

Trammo DMCC, Transammonia’s Dubai-based subsidiary, and ASOE Chile Diez SpA signed a Memorandum of Understanding (MOU) for an exclusive green ammonia offtake of the entire output of the facility (GM May 21, 2021). The project was initially started by Austria Energy Group and Ӧkowind with CIP joining the joint venture in 2022 (GM Jan. 21, 2022).

Energie Baden-Württemberg (EnBW) has begun marketing 100,000 mt/y of green ammonia from the Skipavika Green Ammonia (SkiGA) project in western Norway. The volumes are planned to be available starting in 2027 to be transported to various delivery locations including the Skipavika port or terminals in Western Europe. Interested companies can bid for the capacity on the EnBW website.

SkiGA is a joint venture between developer Fuella AS and Skipavika Innovation. EnBW entered cooperation with Fuella in 2023 with a 10% equity stake to support the investment decision and secure exclusive rights to a long-term offtake agreement.

The SkiGA project is one of Europe’s first emission-free green ammonia facilities, built using local green electricity. It is expected to produce 300 mt/d of green ammonia from renewable electricity generated by wind and hydro power. A Power Purchase Agreement (PPA) for up to 130MW of renewable power for 15 years was negotiated by Fuella AS with power producer Hafslund for the project in April (GM April 19, p. 25).

The Energy Market Authority (EMA) and the Maritime and Port Authority of Singapore (MPA) have shortlisted two consortia to proceed to the next round of proposal evaluations to provide a low or zero-carbon ammonia solution for power generation and bunkering on Jurong Island.

The two consortia leads that have been selected from a total of six are Keppel’s Infrastructure Division and Sembcorp-SLNG. The bunkering players include Itochu Corporation, Nippon Yusen Kabushiki Kaisha, and Sumitomo Corp.

These consortia will conduct engineering, safety, and emergency response studies for the proposed project. After selection, the leading developer will develop an ammonia solution that generates 55-65 MW of electricity from low or zero-carbon ammonia via a Combined Cycle Gas Turbine, as well as ammonia bunkering capacity of 100,000 mt/y. The lead developer will be announced in 1Q 2025, according to MPA’s press release.

As part of Singapore Green Plan 2030, the Singapore government announced the “Sustainable Jurong Island” initiative to transform Jurong Island into a sustainable Energy and Chemicals (E&C) Park (GM Oct. 28, 2022).