Fertilizer Futures

Yara International ASA reported a 46% decline in adjusted EBITDA for the fourth quarter ended Dec. 31, 2023, to $576 million from $1.07 billion a year earlier, beating the average analyst estimate of $373.8 million (Bloomberg Consensus). Yara shares jumped as much as 7.9%, their largest intraday rise since 2020.

Net income attributable to shareholders of the parent was $244 million for the quarter, a 68% drop on the year-ago $769 million. Adjusted earnings per share were $0.88 against $2.46 per share a year ago. Fourth-quarter revenue was down 34% year-over-year, to $3.58 billion from $5.46 billion.

Yara said its results were impacted by significantly lower market prices and one-off position effects. To protect its margins amid subdued demand, the company curtailed some of its European production in the fourth quarter, equating to 11% of both finished fertilizers and ammonia capacity.

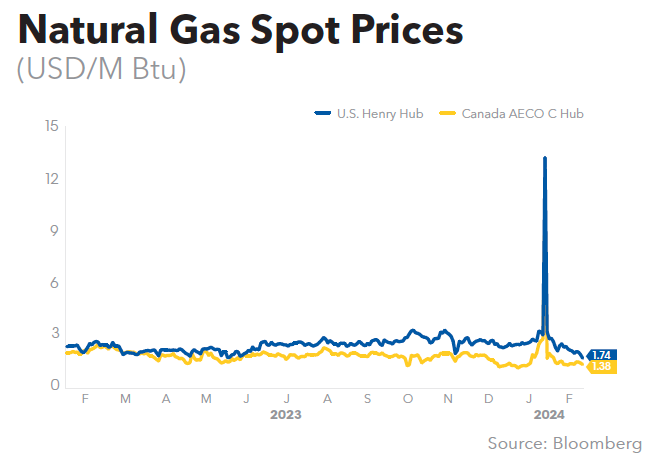

Many fertilizer plants were forced to shut or curtail production in 2022 as costs surged for natural gas. While prices have since retreated, the profitability of European producers is still under pressure. Yara pointed to the improving trend since the second quarter, however, and a positive market trend going into 2024.

“So far this season, nitrogen supply is lower than normal both in Europe and the US, indicating a tighter global balance for the first half of 2024,” said Yara International President and CEO Svein Tore Holsether in a company’s Feb. 9 earnings release.

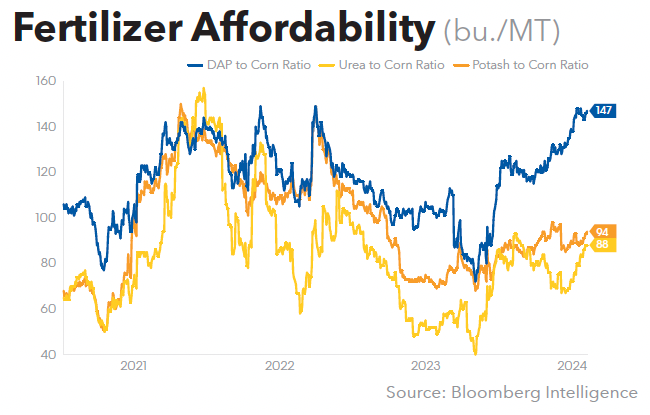

“Fertilizer affordability has improved during the quarter, and optimal application rates for wheat in Europe are currently around 6% higher than a year ago,” Holsether continued. “The start of 2024 has seen increased buying activity and higher prices, signalling a potential volume catch-up into the main application season in the Northern hemisphere.”

Based on current forward markets for natural gas as of Jan. 31, 2024, and assuming stable gas purchase volumes, the company sees its gas cost for the first and second quarters of 2024 at an estimated $320 million and $100 million lower, respectively, than a year earlier.

Yara’s fourth-quarter ammonia production was 19% higher year-over-year, at 1.87 million mt versus 1.57 million mt. Production of finished fertilizer and industrial products, excluding bulk blends, was up 12% at 4.93 million mt versus the year-ago 4.40 million mt.

Crop nutrition deliveries in the fourth quarter were 4% higher than the prior year at 5.32 million mt versus 5.11 million mt. Crop nutrition deliveries increased for all regions except in Brazil and other Latin America and in Africa.

Deliveries increased by 6% in Europe, to 1.76 million mt versus 1.66 million mt in fourth-quarter 2022, which was impacted by a high-price environment and production curtailments. Overall Americas deliveries were down 1% year-over-year, to 2.38 million mt. Brazil deliveries were off 2%, at 1.38 million mt, due to reduced fertilizer demand in the second corn season, partly offset by increased commodity sales.

Industrial product deliveries were 8% lower than in fourth-quarter 2022, to 1.51 million mt from 1.65 million mt. The downturn was mainly in the chemical applications Europe and mining applications. Clean ammonia deliveries were down 10% from the prior year, with Yara citing a “distinct lack of downstream industrial and fertilizer demand.”

For the full-year 2023, Yara posted a 65% decline in adjusted EBITDA, to $1.71 billion from the prior year’s $4.89 billion. Revenue was down 35% year-over-year, to $15.55 billion from $24.05 billion. Full-year net income attributable to shareholders of the parent was $48 million against a net income of $2.78 billion for FY2022. Adjusted earnings per share were $1.11 versus $10.98 for full-year 2022.

Yara declared a dividend of NOK5 per share for 2023. This compares to a dividend of NOK55 for 2022.

Norne analyst Tomas Skeivys, as cited by Bloomberg, noted Yara’s positive outlook comments, adding that he is looking to “slightly raise” his EBITDA and revenue estimates. He sees volumes as likely picking up in the first half of 2024 and gas costs continuing to decline. However, Skeivys flagged Yara’s “rather weak” revenue and cash flow.

Yara Production and Deliveries

| ‘000 mt | 4Q-2023 | 4Q-2022 | FY2023 | FY2022 |

| Production1 | ||||

| Ammonia | 1,871 | 1,568 | 6,391 | 6,510 |

| Finished Fertilizer and Industrial Products (excluding bulk blends)1 | 4,933 | 4,403 | 18,437 | 18,332 |

| Yara Deliveries | ||||

| Ammonia Trade | 422 | 467 | 1,475 | 1,771 |

| Fertilizer | 5,315 | 5,114 | 22,283 | 22,687 |

| Industrial Product | 1,514 | 1,645 | 6,350 | 7,159 |

| Total Deliveries | 7,251 | 7,226 | 30,109 | 31,616 |

1 Including Yara share of production in equity-accounted investees, excluding Yara-produced blends

Yara Deliveries

| ‘000 mt | 4Q-2023 | 4Q-2022 | FY2023 | FY2022 |

| Crop Nutrition Deliveries | ||||

| Urea | 1,141 | 995 | 4,690 | 4,700 |

| Nitrate | 1,069 | 1,027 | 4,462 | 4,442 |

| NPK | 2,025 | 2,131 | 8,355 | 8,498 |

| CN | 329 | 323 | 1,478 | 1,500 |

| UAN | 212 | 140 | 1,047 | 998 |

| DAP/MAP/SSP | 118 | 109 | 560 | 559 |

| MOP/SOP | 176 | 149 | 709 | 921 |

| Other products | 246 | 240 | 982 | 1,069 |

| Total Crop Nutrition Deliveries | 5,315 | 5,114 | 22,283 | 22,687 |

| Europe Deliveries | 1,760 | 1,661 | 7,705 | 7,455 |

| Americas Deliveries | 2,382 | 2,414 | 10,073 | 10,943 |

| North America | 646 | 641 | 2,811 | 2,814 |

| Brazil | 1,377 | 1,406 | 5,619 | 6,450 |

| Latin America excluding Brazil | 359 | 367 | 1,642 | 1,679 |

| Africa & Asia Deliveries1 | 1,174 | 1,039 | 4,506 | 4,289 |

| Asia | 876 | 721 | 3,373 | 3,271 |

| Africa | 298 | 318 | 1,133 | 1,018 |

| Industrial Solutions Deliveries | 1,514 | 1,645 | 6,350 | 7,159 |

1 The Africa and Asia business also includes Oceania

India on Feb. 6 reported that seven ships carrying fertilizer to the country have been rerouted from the Red Sea so far due to disturbances, according to the Press Trust of India. Major shipping companies are warning that the security situation in the Red Sea continues to deteriorate despite efforts by the west to limit attacks by Yemen’s Houthi rebels, according to Bloomberg.

The bosses of A.P. Moller-Maersk A/S and D/S Norden A/S said on Feb. 8 that they felt the threat level was continuing to escalate in the region. It comes after Japanese shipping giant Mitsui OSK Lines Ltd. (MOL) said the disruption on the route could last for a year.

Swaths of the merchant fleet have been avoiding the waterway since attacks by the Houthis began in mid-November. The area grew even more volatile after the US and UK launched airstrikes last month, prompting major owners in all sectors to avoid the region.

“We’ve not seen the level of threat peak, to the contrary,” Maersk CEO Vincent Clerc said in a Bloomberg TV interview. “The amount or the range of weapons that are being used for these attacks is expanding and there is no clear line of sight to when and how the international community will be able to mobilize itself and guarantee safe passage for us.”

The shipping companies’ perceptions of risk matter because they will dictate when vessels return to the region. All of the owners said they will continue to reroute ships until it is safe to travel the Red Sea.

In addition to the airstrikes launched by the US and UK, there is also a defensive force operating in the Red Sea known as Operation Prosperity Guardian. Military ships in the region have been attempting to thwart missile strikes on merchant vessels over the past few weeks, but the Houthis have continued their attacks. There has also been a parallel uptick in Somali piracy.

Norden CEO Jan Rinbo said there needs to be signs of a period of stability with no further attacks before shipping companies will think about returning. “You need to have a de-escalating situation, and we are not at that point yet,” he said. “If anything, it just seems to escalate.”

Clerc said Maersk will continue to reroute its ships around Africa for several more weeks and has previously said the company would need to be “absolutely certain” the waterway was safe before sailing there again. MOL said its diversions will continue for at least the next two to three months, while Norden said it doesn’t expect an imminent resolution.

At the same time, dry weather has forced the Panama Canal – one of the world’s other vital maritime chokepoints – to reduce traffic due to low water levels, also forcing a large number of ship diversions.

“That really is unprecedented,” Norden’s Rindbo said. “I’ve not in my 29 years in shipping seen anything like this.”

CF Industries Holdings Inc. on Feb. 5 announced that Christopher D. Bohn has been appointed Executive Vice President and Chief Operating Officer and has been elected to the company’s Board of Directors, effective Feb. 1, 2024. He will lead global manufacturing, distribution, sales, and supply chain, including CF’s clean energy initiatives. He will be accountable for operational excellence focused on safety, productivity, and long-term growth.

“Chris has experience leading most areas of our business and has been instrumental in developing and growing our clean energy strategy,” said Tony Will, CF President and CEO. “He will continue to drive operational excellence across the organization while managing a range of complex growth initiatives. This promotion and his election to the Board recognize his strong leadership and future contributions to CF Industries.”

Bohn is currently Executive Vice President and CFO with responsibility for strategic planning, business development, and investor relations. He previously served as Senior Vice President, Manufacturing and Distribution; Vice President, Supply Chain; and Vice President, Corporate Planning. He joined CF in September 2009, and has more than 14 years of experience in the nitrogen fertilizer sector.

Bohn will continue to serve as CFO until a permanent replacement has been appointed. An external search is underway.

Iowa legislators have joined the debate over the $3.6 billion deal in which Koch Industries Inc. would buy OCI Global’s Iowa Fertilizer Co., which has a nitrogen plant in Wever (GM Dec. 22, 2023). They follow Iowa State Auditor Rob Sand’s opposition to the deal (GM Feb. 2, p. 1), as well as that of some 18 agriculture and environmental groups (GM Jan. 26, p. 1).

“I am highly concerned about the $550 million in taxpayer incentives that were given away to increase competition in the fertilizer market that may now serve to the benefit of one of the largest players in that industry,” Iowa Representative Elinor Levin (D) told Green Markets. “Monopolies hurt Iowans, and our job is to help make Iowans’ lives better. We are simply asking other entities, including our AG, to do the job they are authorized to do by investigating the deal.”

Levin, along with Rep. J.D. Scholten (D), also weighed in with KBUR news radio in a Feb. 6 broadcast. “Ask any rowcrop farmer and fertilizer is one of the number one costs they’ll bring up as an issue,” Scholten said in the broadcast. “This issue is not new and this is what Governor Branstad did when he gave tax breaks to Iowa Fertilizer Co. over 10 years ago to create competition in the market.”

On the other side of the debate, Iowa State Senator Jeff Reichman (R) issued a statement to local media saying he was personally excited by the deal.

“Only ivory tower liberals would object to an American company purchasing a plant from an Egyptian company,” he said, adding that Koch Industries has a history of growth and investment that should be cause for excitement in southeast Iowa. He said Auditor Sand’s position was grandstanding and a slap in the face to southeast Iowa.

“Rob Sand is so beholden to the crazy coastal liberals obsessed with Koch Industries, he had to pander to them by opposing the sale of the fertilizer plant from OCI to Koch Industries,” Reichman said. “In the process, he showed he’s just another run-of-the-mill liberal despite his attempts to cast himself as something different.”

“Democrats have always opposed the fertilizer plant because they want to put government first, no matter how many jobs the project created,” Reichman added. He said their opposition to the plant contributed to them losing every legislative seat in southeast Iowa since construction started.

Representatives from the Russian port city of Arkhangelsk and the Belarusian government have held talks about the potential of creating a specialized terminal for the transshipment of Belarusian cargo, in particular potash, Interfax reported.

Arkhangelsk lies within the Arctic Circle, more than 1,000 kilometers from Moscow. Belarus is interested in the possibility of using Arkhangelsk for cargo transshipment, given that its port allows access to the ocean without crossing the territorial waters of other states, Interfax reported, citing Arkhangelsk Mayor Alexander Tsybulsky.

The Russian government earlier approved a program for the accelerated development of the Arkhangelsk transport hub through 2035. The program provides an infrastructure project to construct a deep-water area that will be able to accept ships with a draft of up to 15 meters and handle cargo year-round. The port currently requires the deployment of icebreakers to remain navigable during the winter months.

Since the imposition of Western sanctions, Belarus has been forced to reorient the transshipment of its export cargo to Russian ports and has also increased exports to China by rail. Belarus currently ships the lion’s share of its seaborne potash volumes through the port of St. Petersburg (GM June 23, 2023).

Belarus still has plans to build a port near Murmansk in northwest Russia to handle its potash and fertilizer shipments, according to Murmansk Oblast Governor Andrei Chibis speaking to Interfax in December (GM Dec. 15, 2023). Chibis said the current proposal is a request from Belarus for a separate port with a transshipment capacity of 5-7 million mt/y.

Belarus is also reported to be looking at the possibility of establishing logistics corridors and routes to India through Russia and Iran, according to a Tass report, citing Dmitry Krutoy, the Belarusian ambassador to Russia. The aim is reportedly to find an effective average tariff for delivery to Astrakhan, a seaport situated on the delta of the Volga River, some 100 kilometers from the Caspian Sea, and for transportation to Iran’s Caspian seaports for shipment across Iran and possibly ending with a corridor to India.

Krutoy reiterated the importance of the Indian market to Belarus. India imported 992,377 mt of potash from Belarus in 2021, according to Trade Data Monitor, the last full year before Western sanctions started to bite. India’s potash imports from Belarus fell to 383,566 mt in 2022.

Belarus and Iran last year agreed on the supply of 400,000 mt of Belarusian potash, though neither the delivery period nor how much of the volume would be consumed in Iran was disclosed (GM Nov. 10, 2023). Iran consumed just 20,000 mt of potash in 2022, according to IFA data, and sources believed the bulk of the 400,000 mt was destined for other markets.

Belarus began reorienting transshipments of its potash exports after Lithuania’s government terminated the railway transit contract between the country’s state-owned railway company Lietuvos Geležinkeliai (LTG) and Belaruskali as of Feb. 1, 2022, over national security concerns (GM Jan. 14, 2022). The Lithuanian government’s decision came in the wake of EU and US sectoral sanctions on Belarus.

The removal of the Lithuanian rail route effectively blocked Belaruskali’s key export route. Before the imposition of Western sanctions, the Belarus producer and its marketing/export arm, Belarusian Potash Co. (BPC), shipped 10-11 million mt of potash annually through the Lithuanian port of Klaipėda.

Compass Minerals posted a $75 million loss for the first quarter ending Dec. 31, 2023, citing a total of $77.3 million in impairment and restructuring charges from terminating its lithium business. Compass announced the termination and loss on Feb. 7. Compass’ year-ago loss was $300,000.

“The environment surrounding our lithium project today is markedly different than the one that existed a couple of years ago when we started down this path,” said Compass President and CEO Edward Dowling, who took the helm on Jan. 18 (GM Feb. 2, p. 24) after nearly two years on the Board of Directors.

“The simple fact is that the regulatory risks have increased significantly around this project,” Dowling said. “When combined with other changes to the commercial landscape, it became clear that the risk-adjusted returns on this project are inadequate to justify the investment.”

Compass said last May that it was concerned by recent legislative actions in Utah that altered certain aspects of the regulatory regime that would govern lithium development at the lake, some of which would require rulemaking (GM May 12, 2023).

Citing the need for clarity in the evolving regulatory climate in Utah, Compass indefinitely suspended any further investment in the lithium project last November. Compass said a proposed rule published by the Utah Division of Forestry, Fire and State Lands, in mid-October introduced new obstacles to lithium salt production in the Great Salt Lake.

In addition to the regulatory risk, Dowling also noted concern with doing a project with a technology that has yet to be successfully deployed. As a result of the termination, the lithium development team has been disbanded, and Chris Yandell, Head of Lithium, has left the company.

“I want to thank Chris and the exceptional team he assembled for their efforts to advance the project over the last couple of years. We wish those who are leaving the company the best in their future endeavors,” Dowling said.

“I will note that the lithium content in the Great Salt Lake is a significant resource that’s not going anywhere,” Dowling added. He said the company will continue to monitor and engage in appropriate legislative and regulatory processes in Utah, as well as watch emerging commercial developments to preserve the long-term optionality of that resource.

In a Feb. 8 earnings call, Dowling also addressed the recent departure of former President and CEO Kevin Crutchfield.

“As you know, the last year has been a challenging one for Compass,” Dowling said. “Ultimately, the Board and Kevin agreed that a change in leadership was in the best interest of the company. This change allows employees and the investment community to refocus on our advantage assets that underpin our core salt and plant nutrition businesses, as well as the emerging and exciting fire retardant business.”

Dowling thanked Crutchfield for this leadership and said he attained the three major goals that the Board set for him when he joined the company in 2019: fix the challenging production curve at the Goderich salt mine and repair significantly strained relationships at the mine; exit South America; and determine if there were any areas of growth adjacent to the company’s core salt and plant nutrition businesses.

“We are refocusing our efforts on improving cash flow generation and returns on capital in our core Salt and Plant Nutrition businesses through rigorous cost management and reduced capital intensity,” Dowling said. “Over many decades, our company has developed an exceptional set of unique assets that are virtually irreplicable, enjoy durable competitive advantages, and have strong leadership positions in the marketplace.”

Compass reported a first-quarter operating loss of $55.3 million on revenue of $341.7 million, compared to the year-ago income of $27.9 million and $352.4 million, respectively. Adjusted EBITDA was $59.4 million, down from $61.8 million.

The Plant Nutrition segment posted an operating loss of $2.3 million on sales of $49.7 million, compared to the year-ago income of $11 million and $41.6 million, respectively. EBITDA was $6.1 million, down from $19.3 million.

Fertilizer sales volumes were up 67%, to 75,000 st from the year-ago 45,000 st, reflecting higher demand and historical norms in the company’s core West Coast markets. However, prices were down 29%, to $660.41/st from the year-ago $924.15/st, with the company citing excess supply in the global potassium-based fertilizer market.

Compass has adjusted its 2024 annual guidance for the Plant Nutrition segment to reflect revised market and operational conditions that could impact the business. Sales volumes are now put at 280,000-310,000 st versus the previous 290,000-320,000 st; revenue at $170-$205 million versus $180-$215 million; and adjusted EBITDA at $15-$35 million versus $20-$40 million.

Compass noted that muriate of potash (MOP) prices continue to be under pressure, which as a potential substitute, impacts the price of the company’s sulfate of potash (SOP). It also said the continued weakness in fertilizer prices is resulting in buyers deferring purchases in anticipation of lower prices.

In addition, first-quarter pond-based production tracked toward the lower end of the company’s initial projections. Lower production means the company has to buy more MOP to supplement its SOP production.

Despite first-quarter winter weather that was “exceptionally weak,” operating income was still up in the company’s Salt segment, to $50.5 million on sales of $274.3 million compared to the year-ago $47.1 million and $308.1 million, respectively. EBITDA was up at $65.7 million from the year-ago $61 million. While total salt volumes were off at 2.86 million st from the year-ago 3.52 million st, average prices were up at $96.08/st from $87.51/st.

Compass has left 2024 guidance for the Salt and Corporate segments in place. Salt volumes are put at 11.3-12.15 million st, revenue at $1.03-$1.11 billion, and adjusted EBITDA at $230-$270 million, with mild or strong winters altering those numbers.

Compass said its Fortress North America fire retardant business recognized slightly better results related to the take-or-pay provisions of its calendar year 2023 contract with the US Forest Service in the first quarter, with operating earnings and adjusted EBITDA of $13.1 million. Negotiations for the 2024 contract continue and are expected to be finalized prior to the upcoming fire season. Compass will adjust guidance once the contract is complete.

US farmers are poised this year to see the biggest hit to their income since 2006 as a slump in agriculture markets takes its toll, according to Bloomberg. Net farm income is forecast to fall about 26% in 2024, to $116.1 billion, according to USDA data released on Feb. 7. If the estimate holds, it would mark the biggest year-over-year drop since 2006.

The outlook is the agency’s first for the calendar year and comes after net farm income already fell about 16% in 2023. Prices for major crops have slumped amid plentiful supplies. At the same time, American farmers have started to lose their dominance in global grain shipping as Brazil strengthens its position.

The expected decline for income in 2024 puts profits below the 20-year average of $118.2 billion, according to USDA. Direct government farm payments are expected to drop almost 16% from last year. Cash receipts are also seen decreasing, while total production expenses are expected to rise 3.8%.

PhosAgro PJSC reported a 2% growth in its agrochemicals output in 2023, to a record 11.28 million mt from 11.07 million mt the previous year, and in line with the output guidance given by the group in early December (GM Dec. 8, 2023).

Fertilizer output in 2023 totaled 10.99 million mt, also up 2% year-over-year, while production of other agrochemicals was down 5% from 2022, to 286,000 mt.

PhosAgro said the growth in its fertilizer output was driven primarily by an 8% increase in DAP and MAP production, to more than 4.5 million mt. MAP output alone increased by 13%, largely driven by the ramp-up at the group’s Volkhov complex in southern Russia (GM Sept. 1, 2023). A 4% rise in ammonium nitrate production and a 2% increase in urea output, to 723,000 mt and 1.7 million mt, respectively, also helped boost the group’s 2023 output.

PhosAgro also highlighted a 2% year-over-year increase in the production of key feedstocks, mainly due to a 5% increase in the production of phosphoric acid and a 3% rise in sulfuric acid production, to 3.3 million mt and 8.1 million mt, respectively. The increase in sulfuric acid output was driven by improved operational efficiency at the Cherepovets unit and the launch of a new unit at the Balakovo site late last year.

PhosAgro said in December that it plans to boost production by 1.4 million mt/y by 2026 versus the current level (GM Dec. 8, 2023).

PhosAgro Production Volumes

| ‘000 mt | FY2023 | FY2022 | % change |

| Fertilizers | |||

| Phosphate Fertilizers | 8,388.7 | 8,224.4 | +2 |

| Nitrogen Fertilizers | 2,605.3 | 2,546.6 | +2 |

| Total Fertilizers | 10,994.0 | 10,771.0 | +2 |

| Other Products | |||

| STPP | 55.7 | 68.3 | (18) |

| Other | 230.3 | 233.6 | (1) |

| Total Other Products | 286.0 | 301.9 | (5) |

| Total Agrochemical Products | 11,280.0 | 11,072.9 | +2 |

| Feedstocks | |||

| Ammonia | 1,982.8 | 1,985.3 | (0.1) |

| Phosphoric Acid | 3,345.3 | 3,199.4 | +5 |

| Sulfuric Acid | 8,120.0 | 7,920.2 | +3 |

| Ammonium Sulfate | 260.2 | 322.6 | (19) |

| Total Feedstocks | 13,708.3 | 13,427.6 | +2 |

Increased production and productivity were one of the critical factors in PhosAgro’s decision to index the wages of the group’s employees from Feb. 1, 2024, by a further 15% in addition to the 60% increase in average wages from 2021 through 2023, PhosAgro CEO Mikhail Rybnikov reported on Feb. 6.

The group earlier reported that it exported 8.7 million mt of fertilizers in 2023 based on preliminary data, a 1% increase on 2022’s export volume of 8.6 million mt (GM Jan. 5, p. 26). PhosAgro’s nitrogen fertilizer exports increased 6.5% year-over-year, while phosphate exports rose 8.7%.